Yes, it’s been quite awhile. I thought it better to do a deeper dive on the issues addressed in this blog and to publish the findings in book form. Full-length books, just in time for that period in history when people won’t read anything longer than a tweet! Oh well.

The plan is for a series of three books, the first of which is now available as a free downloadable PDF at the link. Books 2 and 3 are works in progress. A quick summary of the series:

A diagnosis of our money system: Precisely how it is designed, from the ground up, to guarantee that it is a system of struggle for the vast majority of people on the planet, ensuring that we have:

accelerating income inequality;

widespread debt slavery for so many people, businesses, and almost all governments;

perpetual price inflation;

perpetual financial crises;

people running ever faster yet feeling they don’t have enough time, especially for what is most important to them;

domination by Big–Big banks, Big corporations, Big political parties, Big government agencies;

addiction to financialized economic “growth” no matter what the consequences for people and nature;

perpetual conflict among people and nations;

and so forth.

In other words, it’s a comedy! (OK, it’s not a comedy, but it seemed that at least a little levity was called for after that list.)

Book 2:Value the Valuable!

Solutions: How we start turning the economic ship so it helps the many, not just the few.

Book 3:Vanquishing Financial Problems Once and for All

A treatment of these topics from the energetic / meditative / spiritual / psychological point of view.

This is likely the first of the final three posts on this blog. There will be a post here when each of the three books is released.

There’s no catch. As on Thundering Heard, the book The Debt Standard: How our money system plagues our world is free. We don’t do any tracking of individual visitors. You don’t even have to supply an email address to download the book. Though you can leave your email address at the Contact page at the new web site Debt-Standard.com if you want to submit any comments or questions about the book, or to receive occasional email updates.

Thank you very much. I am grateful for your time and attention!

Most people likely heard that on December 15, the US Federal Reserve raised interest rates for the first time in nine years. Nine years! And by a measly 1/4 of a percent. With high Madison Avenue puffery, they called this “liftoff”! And why now? Because, they claim, finally, after telling us at the end of every year, for the last six years, that the economy would accelerate in the new year and be able to grow on its own without their “extraordinary measures” (their phrase, not mine) of support, they are declaring, like Bullwinkle, “This time for sure!”

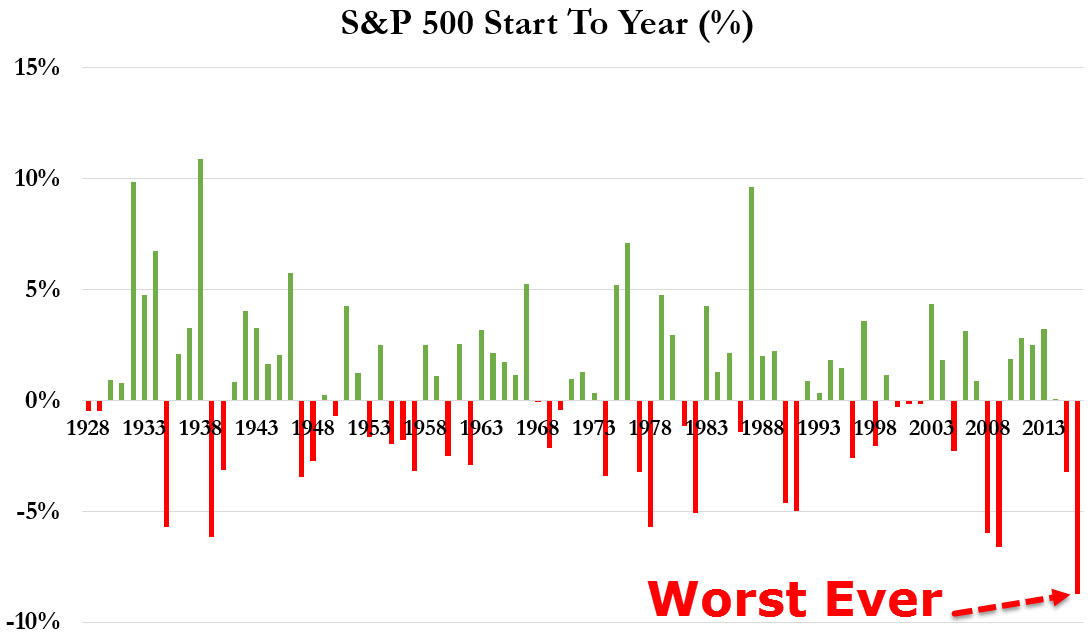

Stock markets are, of course, throwing a tantrum, off to their worst start to a new year ever, screaming, “What?! No more free money for the rich?! You mean we’ll actually have to do something to get money, like–uuuugh–poor people do?”

Worst start ever for other countries as well, including Europe as a whole. The 600 largest European stocks (EuroStoxx 600) are down 21% from their peak in April, officially qualifying them for a bear market. Same with China, their stocks lost 21% in the last four weeks (since the Fed raised rates) and are down 44% since their peak in June:

Stocks in emerging market countries (Brazil, Thailand, South Korea, Malaysia, etc.) peaked in Autumn 2014 (!) and are down 36% since then. This was posted in August:

Still, many people, especially in the US, believe we are in a global bull market in stocks; despite the fact that US smaller company stocks (Russell 2000 index) are down 22% since their peak in June, 2015. And US Transportation stocks (truckers, airlines, shippers, etc.), which are an excellent barometer of economic activity, are down 28% since their peak.

Even in the midst of this stock market tantrum, a desperate US President said last week that everything is awesome and that “Anyone claiming that America’s economy is in decline is peddling fiction.” Forget about those 45 million US residents on food stamps, and a record number of homeless children, everything is supposedly great. And there was this desperation from the Fed on Friday:

January 15 – Bloomberg (Matthew Boesler): “The U.S. economy should continue to grow faster than its potential this year, supporting further interest-rate increases by the Federal Reserve,” New York Fed President William C. Dudley said. ‘In terms of the economic outlook, the situation does not appear to have changed much since the Fed’s Dec. 15-16 meeting,’ Dudley said, in remarks prepared for a speech Friday… He added that he continues ‘to expect that the economy will expand at a pace slightly above its long-term trend in 2016…’

(Digression: Only someone involved in pseudo-scientific economics is typically deranged enough to try to explain how something can “grow faster than its potential.” Perhaps we should each send our favorite economist a dictionary.)

Why do I call these statements desperation?

For starters, the Federal Reserve’s best computer model for the economy says that the economy is growing at a 0.6% annual rate. That’s less than 1% a year, folks. In other words, stall speed.

JP Morgan says it’s less than that. They expect 0.1%:

I’ve talked here before about the usefulness of economic statistics that governments don’t publish since the governments can’t fake them. I won’t bore you with a lot of them, but here’s one that will give you an excellent idea of the state of things. It shows, over the last 30 years, the cost to companies to transport bulks goods (wheat, copper, coal, oil, iron ore, etc.) by cargo ship around the planet:

The first thing to notice is that it costs less to ship cargo now than it has at any time in the last 30 years. And it’s cheaper by a wide margin. If the economy were doing well, cargo ships would be in high demand and charging high prices. That’s hardly the case now; quite the opposite.

Next, check that blue oval at the top of the chart. The index was over 10,000 in early 2008. That was a period of high demand for shipping. It’s useful to know that owners of large ocean-going cargo vessels currently break even when the price they can charge for shipping is between 800 and 1,000 on this index. So with shipping costs as high as they were in 2008, the owners of ships were making a LOT of money–they could charge more than 10 times their expenses for fuel, salaries, maintenance, etc. Now the price is below 400. So the ship owners lose money on every shipment. Competing owners of cargo ships continue to ship at these low prices, even though they are losing money, because they hope their competitors will go bankrupt before they do.

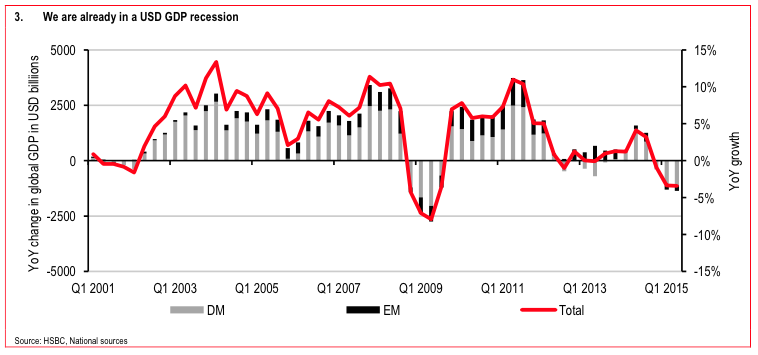

Why is it so cheap to ship goods around the world now? Because global trade and the global economy are tanking, and far fewer goods are being shipped than a few years back. Here’s a chart by HSBC of growth of the global economy calculated in US Dollars. Notice that the line is well below zero for 2015, just like it was in 2009:

Credit Suisse expects Brazil’s economy to have its worst downturn since 1901! That’s right, worse than the Great Depression. As shown by the chart at the link, India’s exports and imports both crashed by 25% over the last year.That’s a huge decline.

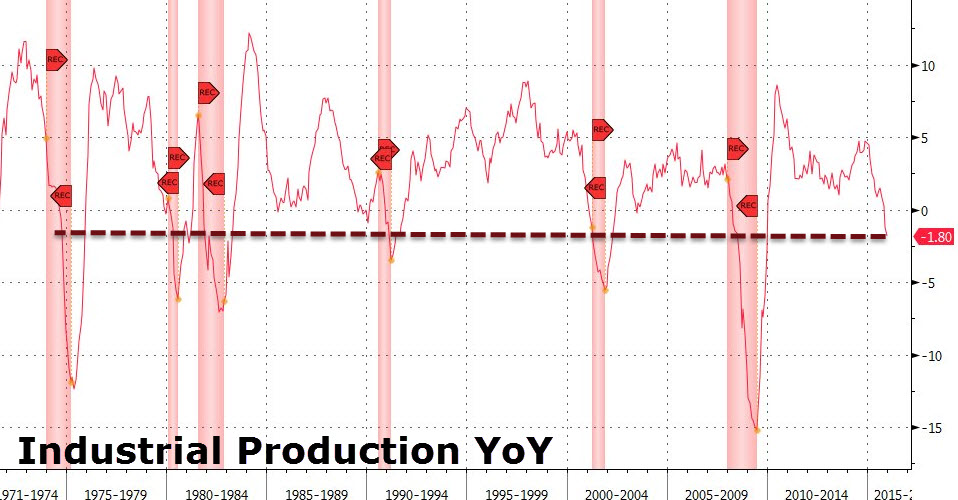

So the Fed and other cheerleaders might say: Yes, the world economy is down, but the US has “decoupled” from the world and is doing fine on its own. Well, here’s a perfect depiction of the US economy. It’s a chart of US Industrial Production over the last 45 years:

Industrial Production in the US is down over the last year; there’s 1.8% less of it than a year ago. The red-shaded areas on the chart are past recessions. As the dashed line shows, whenever Industrial Production has been this low in the past, we have always already been in a recession. Always. No exceptions.

Governments (and 99 out of 100 economists) announce recessions with a huge lag time. Leading up to the announcement, just when it would help people to be battening down the hatches, they always claim everything is fine and there won’t be a recession, so we should all hold onto our stocks, hold onto our real estate, spend, borrow, and spend some more. Then the long delay in admitting to the recession allows them to say, “Yes, a recession started 10 months ago, but now it’s either over or almost over, so don’t worry, everything is fine. Spend, borrow, and spend some more.”

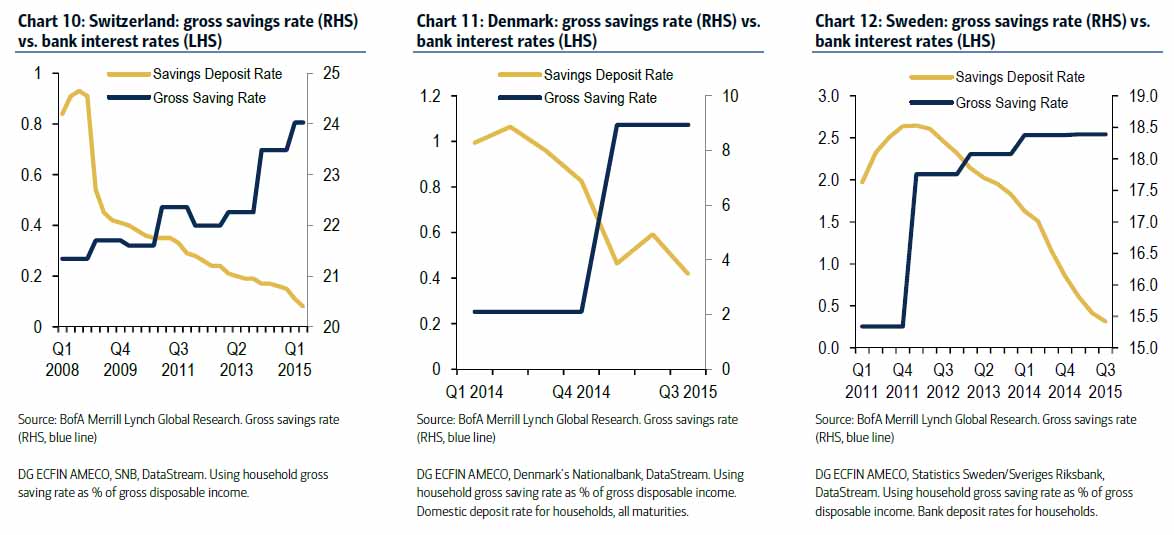

The Fed’s Dudley also said this week that, if the economy weakened, they would consider negative interest rates for the US. Canadian central bankers say the same. And it has worked so well in Europe! (Ha!) Europe’s delusional central bankers thought that negative interest rates would spur people and companies to save less and spend more. What actually happened? Bank of America explained here that as rates went negative and people couldn’t earn interest on their savings, they saved more, not less. In other words, people, unlike the delusional bankers, are being logical: if they can’t earn any interest, then they have to save more for their future plans, not less. Here are the charts showing exactly this relationship (as rates go down, savings go up) for the negative rate champions Switzerland, Denmark, and Sweden:

European business also failed to fall for the negative rates trick. Instead of borrowing and spending more, they have been pulling in their horns and retiring some of their outstanding debt instead of borrowing more.

As Michael Burry of The Big Short said in his speech at UCLA:

The individual can think different and the individual can act different than those that got us all into this mess. No matter how the economic tides may sweep away the majority, an individual can stand clear.

More than ever, it is crucial to understand that “society’s sanctioned suits,” as Burry labels them so well, do not have your best interests in mind. They have their own interests in mind. Period. And their desperation, delusions, and derangements have created an inevitable economic calamity that will be the greatest in history.

People told me they liked the recently-released movie The Big Short based on the book of the same name by Michael Lewis, so I did go to see it at a theater, something I’m loathe to do these days because the theaters seem determined to crush all human sensitivity out of their patrons during the overlong and overloud Coming Retractions segment that precedes the main show. Seems to me that earplugs are a better theater accessory these days than 3D glasses.

Anyway, the movie has been well-received by both critics and audiences. It is a well-crafted dramatization of the true story of a few traders who foresaw the collapse of the housing bubble and figured out how to make large profits from that event. It shows aspects of the lead-up and crash that are not well-known by the public. And it shows the vitriol and threats directed at anyone who sees important events sooner than the general public, especially when what they see means that people are going to lose some or all of their elusive spondulix.

The main character is Michael Burry, who not only foresaw the coming real estate bubble collapse, but had a very good idea of just how devastating it would be for the economy. It’s exceedingly rare for the hero of a movie to be someone as intelligent as Burry.

But more important than the movie is what Burry is doing these days. Remember, Burry does intelligent things before the crowd. He’s a rather private fellow, but has made a few public appearances, one on 60 Minutes, and this one on Bloomberg where he talked about what he was currently buying–farmland with water on site, and gold:

Here is Burry giving a fabulous commencement speech at UCLA in 2012. Burry’s speech starts at the 2:15 into the video:

Selected quotes:

It’s an age of infinite distraction, for those so willing. You are the generation that has had instant messaging, Facebook, Twitter, an angry bird nagging your fingertips at every moment. It’s been arguably as addictive as any drug throughout history, and I do imagine, it took some terrific will power during your studies … to study.

…

In 2010, I published an op-ed in the New York Times posting what I thought was a valid question of the Federal Reserve, Congress, and the President. I saw the crisis coming … why did not the Fed? Never did any member of Congress, any member of government for the matter, reach out to me for an open collegial discussion on what went wrong or what could be done. Rather, within two weeks, all six of my defunct funds were audited. The Congressional Financial Finance Inquiry Commission demanded all my emails and lists of people with whom I conversed going back to 2003, and a little later the FBI showed up. A million in legal and accounting costs and thousands of hours of time wasted – all because I asked questions. It seemed they would pump me at gun point or not at all. That summer the Federal Reserve put out a paper that concluded nothing in the field of economics or finance could have predicted what happened with regards to the housing bust and subsequent economic fallout. Ben Bernanke continues to backfill this logic and I fear that history is being written wrong yet again. The ignorance is willful.

I am shocked that executives at some of the worst lenders were not punished for what they did. But this is the nature of these things. The ones running the machine did not get punished after the dot-com bubble either — all those VCs and dot-com executives still live in their mansions lining the 280 corridor on the San Francisco peninsula. The little guy will pay for it — the small investor, the borrower. Which is why the little guy needs to be warned to be more diligent and to be more suspicious of society’s sanctioned suits offering free money. It will always be seductive, but that’s the devil that wants your soul.

…

The zero interest-rate policy broke the social contract for generations of hardworking Americans who saved for retirement, only to find their savings are not nearly enough. And the interest the Federal Reserve pays on the excess reserves of lending institutions … handcuffed lending to small and midsized enterprises, where the majority of job creation and upward mobility in wages occurs. Government policies and regulations in the post-crisis era have aided the hollowing-out of middle America…These changes even expanded the wealth gap by making asset owners richer at the expense of renters. Maybe there are some positive changes in there, but it seems I fail to see beyond the absurdity.

…

All these people found others to blame, and to that extent, an unhelpful narrative was created. Whether it’s the one percent or hedge funds or Wall Street, I do not think society is well served by failing to encourage every last American to look within.

…

Americans have so much natural entrepreneurial drive. The caveat is that it is technology that should be a tool making lives better in the real world, and in line with the American spirit of getting better and better at something, whether it’s curing cancer or creating a better taxi service. I am less impressed with the market values assigned to technology that enhances distraction.

So folks, do you have your farmland with water on site and some gold? Are you looking within and working like mad to avoid formidable distraction? Or are you following a path designed by what Burry calls “society’s sanctioned suits” offering free money and a million tantalizing distractions?

—That the Greek people would strike a major blow for light in our world! A group of people finally said NO to the reinstatement of debtor’s prisons in which entire countries are placed in such prisons by the Banker Politician Axis known in polite circles as our international financial system. The previous “bailouts” of Greece were not for Greece, they were for the bankers, the lenders:

Yet the Greek people ended up with more debt on their backs and with austerity plans from the “great minds” at the EU, ECB, and IMF that have kept their economy shrinking further each year so that it is now about 25% smaller than in was in 2006. In other words, Greece has been going backwards financially: more and more debt, smaller and smaller economy. Why should they put up with more of this? To their credit, today the people of Greece gave a resounding NO to further strangulation by the EU.

And who could have predicted:

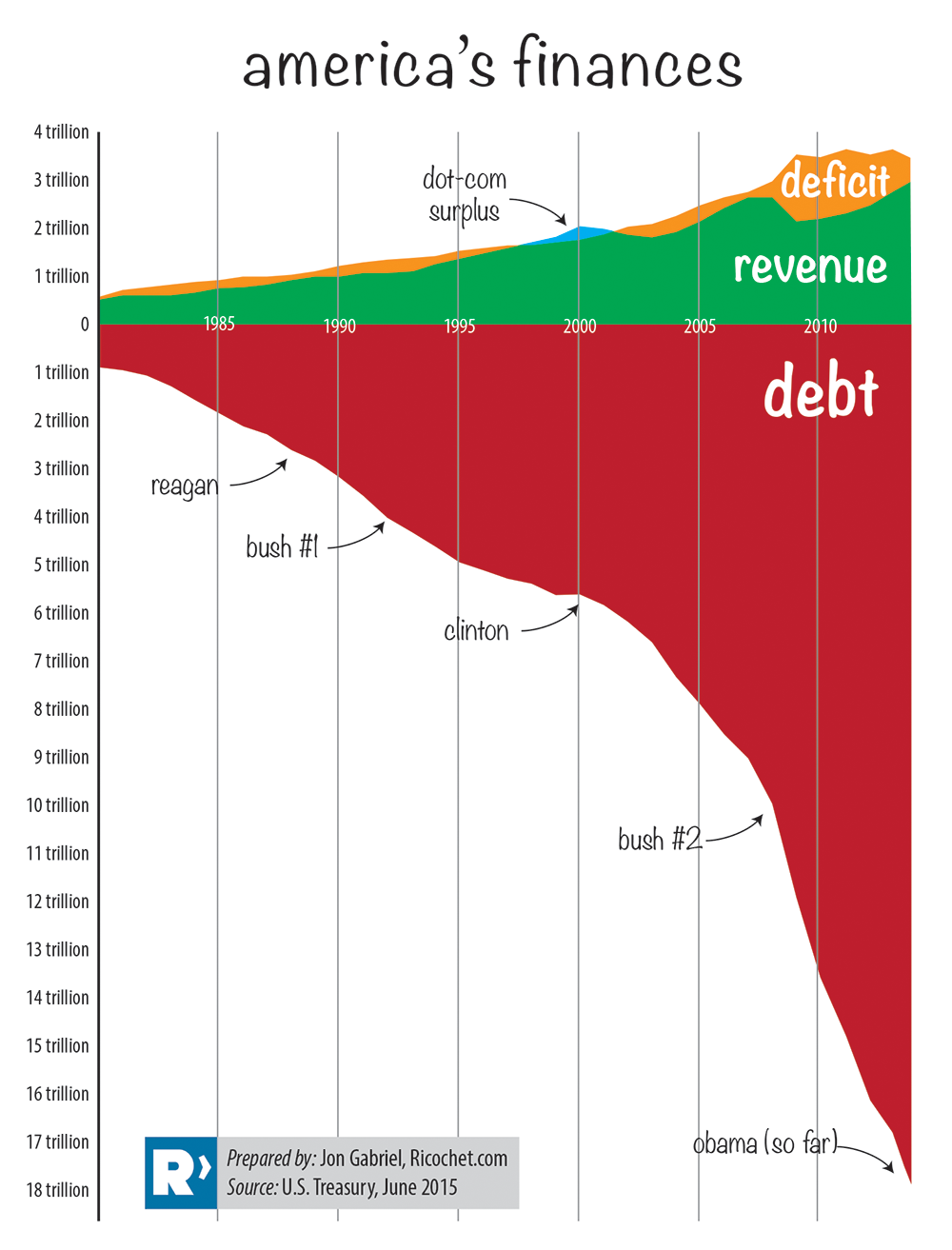

—In the late 1980’s, that Japan Inc. would not take over the world. Starting at the end of 1989, the Japanese economy was revealed to be not an invincible powerhouse but rather a real estate and stock market bubble, the collapse from which Japan is still reeling because—as pointed out repeatedly in the 1990’s and early 2000’s by pontificating central bankers from the West—the Japanese refused to bite the bullet and let the bankrupt go bankrupt and kept zombie banks alive by financial trickery, something the Western central bankers also did starting in 2008 when faced with the same bankruptcy situation of their own banks. And all central bankers (except those in Iceland: they bit the bullet and it worked out far better for them—their debts are now much smaller and their economy is larger than it was in 2007) are still doing exactly that. To keep up appearances, Japan has printed up so much money to buy so much government debt that their national debt is now 19 times annual tax revenues. (Think about that from a person’s point of view. Let’s say the person makes $50,000 per year, and they have to live off that, but they also owe 19 times that, $950,000. How can they ever pay off the debt? Even if they tried to pay off $10,000 per year, the interest on $950,000 at 3% is $28,500, so they would owe $18,500 more every year.) Gee, Japan sounds worse than Greece! Way worse. And here’s a graphic of the US government’s debt:

That looks like it’s going well! Yeah, sure, very sustainable.

And who could have predicted:

—In the late 1980’s, that the USSR would collapse. The USSR was a superpower! But it turned out that the USSR, which made most of its money from commodities such as oil, diamonds, platinum, etc., was unable to withstand the collapse in the prices of all of those commodities in the 1980’s and their entire economy collapsed, taking their overreaching political system down with it. But they hid their problems so well that the CIA incompetently thought the Russian economy was three times larger than it actually turned out to be. Either that or the CIA needed a fake “strong” enemy to boost its own budget.

—In the late 1990’s, that internet stocks would collapse in 2000. It was the new paradigm! If you didn’t believe it, you “just didn’t get it.” Who could have known that Webvan, Pets.com, and EToys.com would go from riches to not even rags?

—In 2007, that real estate prices would collapse. Real estate prices always go up, don’t you know? And they aren’t making any more land! And it’s always a good time to buy! And other lies, too! Tell all that to the 7 million households that were foreclosed upon just in the US in the last decade.

Who could have predicted those things? Well, a few people correctly predicted each of those big changes. But they were generally derided or ignored.

What’s the point of the list? Well, that things change. Sometimes they change in a big way. And sometimes in a hurry:

And we are living in a time about which it’s very easy to argue that we have simultaneous global bubbles in government bonds (think negative interest rates!), stocks (many indexes are higher than they were during previous peaks that were later admitted to be bubbles), and real estate. Don’t think it’s a real estate bubble? This house in San Francisco sold for $1.21 million in March:

It does have one bedroom. And the bathroom is outside! Ah, the fresh air! And the neighborhood is crime-ridden! At least the one in San Francisco was in a good neighborhood, so the $1.21 million was probably for the lot, that is, the house was a knocker-downer, not a fixer-upper.

And with the exponential increase in electronic money printing by governments, it’s easy to argue for a fourth bubble, a currency bubble as well. And people and groups are now making up their own currencies: barter currencies and electronic cryptocurrencies such as Bitcoin. In fact, you can go to sites like CoinCreator.net and create your own cryptocurrency. They claim they’ve created over 4,000 new currencies for people. This site tracks the current price of 653 new cryptocurrencies!

What will be the impact of the Greek vote? The fact that the debt of many (most!) countries is unpayable will now begin to emerge into the mass consciousness. During this latest round of negotiations between Greece and the Troika (EU, ECB, and IMF), the Greek representatives, Varoufakis and Tsipras, have repeatedly tried to explain that the debts of Greece are unpayable, that Greece needs debt relief, debt restructuring. But the Troika played hard ball and said that was out of the question, that Greece had to pay its existing debts fully. But then just over a week ago, someone leaked an internal IMF document that clearly showed that the Greeks were right, that existing Greek debts could never be paid! This allowed Tsipras to go to the people with the backing of that IMF document to urge a NO vote on more strangulation plans from the Troika. Tsipras was able to say, “See, we told you the truth. The Troika knew the truth, but lied about it. Who do you want to trust going forward?”

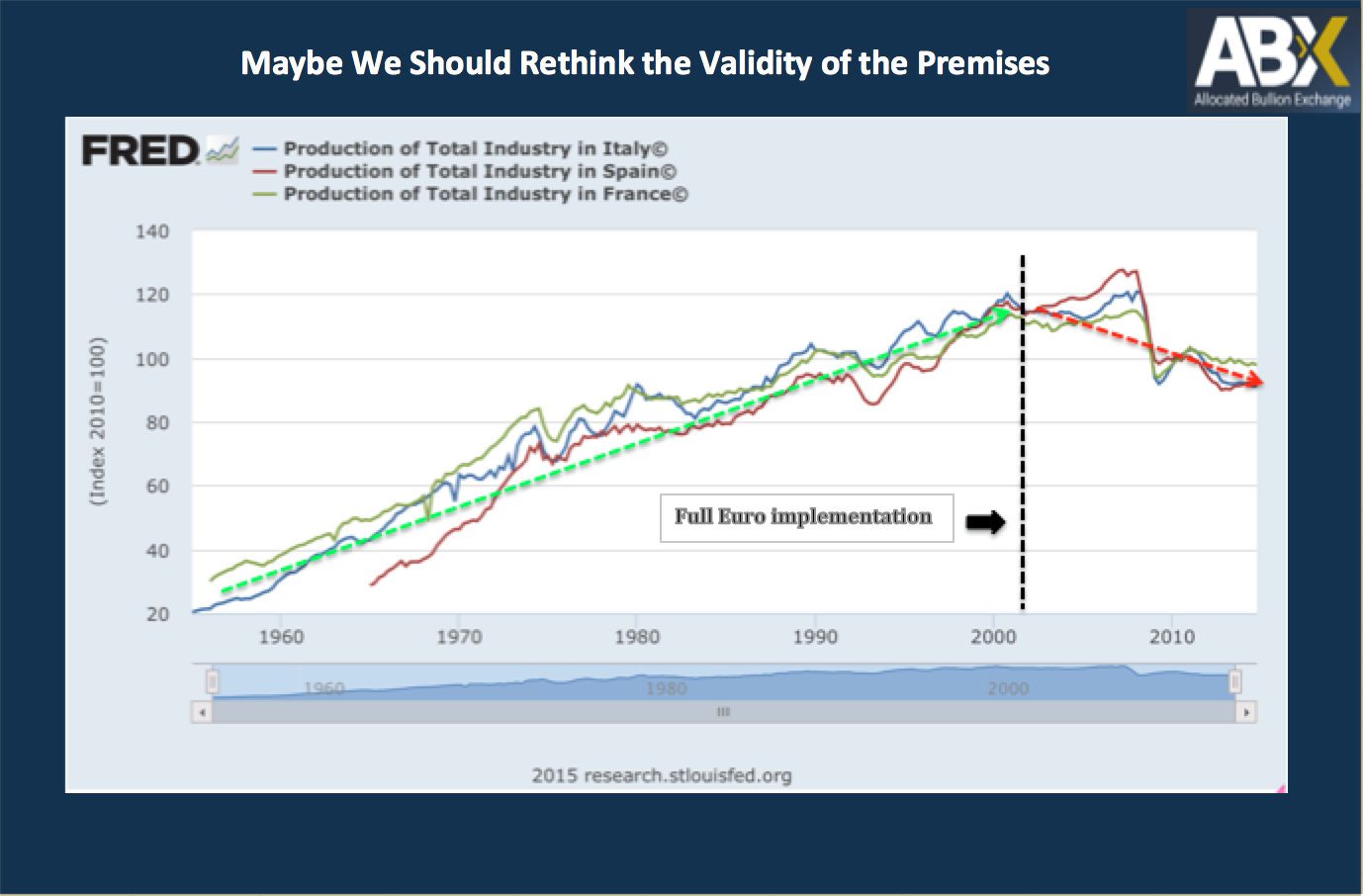

Italy, Spain, Portugal, and France, yes France, come immediately to mind as countries that will never be able to pay their debts. And now that the IMF has admitted the truth about Greece, they will be overrun with requests to show the same for these other countries, all of whom, like Greece, have had rising debts and contracting economies since 2007. This chart shows the 15 to 20% declines in production in Italy, Spain, and, France since 2007:

So the dominoes will now start to fall because these and many other countries have unpayable debts. People will start to understand this.

All we want is truth! Why are these so-called leaders (some of them will be shown in two bonus photos below) so afraid of truth? Well, it was explained well here last week: The truth is that these leaders sold out their own electorates, placing the bad bets of the commercial banks on the backs of their own citizens, making the bankers whole and putting their voters on the hook for unpayable debts. And all of their great plans have been complete failures–except if their plans were to pad banker bonuses. They really don’t want this to be made obvious to everyone in each of their own countries. Getting kicked out of office will be one of their lesser worries.

With the exception of the 2007 event listed above, the other events were mostly local to one country. The one in 2007 almost took down the global financial system. This current bubble-plex (multiple bubbles at once) is global in nature, and will have global systemic consequences. It involves bubbles (debt and currencies) that are the very fiber of the world financial system. The period from September, 2015 through December, 2017 will bring deeper and more dramatic change than most people, even me, can envision. It helps a lot to be ready for change. Inside and outside, some say that preparation is everything.

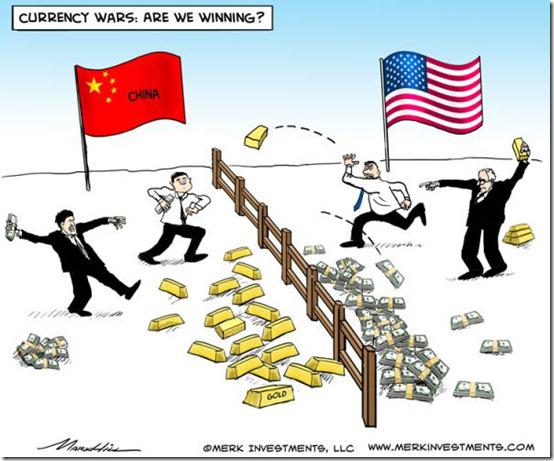

What are the central banks doing about this? Well, they have been printing money to try to fill the holes that have continually been opening up in the system since 2007. What the smarter ones have also been doing since 2007 is buying gold instead of selling it:

China keeps importing around 2,000 tons of gold per year.

I sincerely hope you have been “importing” some as well. Perhaps the US has a (war?) plan to win the game shown in the following cartoon, but at this point, it sure looks like they are losing this game in a big way:

* * *

And as a special bonus, here is a photo of some of these world “leaders” marching “with the people” in France after the Charlie Hebdo shootings. The photos and related videos were plastered all over the mainstream media:

And here’s the reality of that “with the people” thing:

Totally staged! That’s a good description of these people: totally staged.

* * *

And since the Greek people have put me in a very pleasant frame of mind, here’s bonus #2: Make sure not to step in any sinkholes:

And Bonus #3 is a question. The winning answer will receive the first ThunderingHeardBuck created at CoinCreator.net. OK, that’s a joke, but the question is very serious: It used to take generations for people to fall for the next bubble. For many decades following the Tulip Bubble or the South Sea Bubble, people were too smart to fall for a bubble. It took generations for the memory to pass. So the question is: How come we have new major bubbles every seven or so years now?

(Note: As explained here, this is a draft of a chapter from an upcoming book on vanquishing financial problems once and for all. Part 1 provided an overview of the structural unfairness in the system that makes extreme wealth inequality inevitable, and covered how that unfairness is implemented through money creation by banks and taxation. Part 2 covered how money loaned into existence, money designed to lose purchasing power, government borrowing, and governments borrowing their money into existence all play their part in the structural unfairness of the system. This is the final part of the chapter.)

Growth at any Cost

A major consequence of all money being loaned into existence is the growth-at-any-cost mentality that endangers the well-being of all animals and plants on this planet. Very few nations, states, businesses, and individuals are satisfied with a steady-state financial situation. Instead, we are inundated with calls by our so-called leaders for “growth, growth, growth,” chanted like a mantra.

While there is no doubt that economic booms can make people feel good about things (and about those politicians currently in power), it is clear that governments and businesses increasingly resort to desperate tactics when growth seems insufficient and the inevitable recession or depression occurs: businesses slash their employment rolls; governments bust their budgets and borrow vast sums to fund massive “economic stimulus” programs, ignoring whether the money they borrow can ever be repaid; central banks push interest rates—the cost of borrowing (renting) money–to zero or even negative; and central banks resort to what they call quantitative easing (money printing).

The clear source of such desperation lies in the fact that money in this world is debt. If the average interest rate in the world, on all loans, is 4%, then the economy must grow sufficiently (by 4% or more) for everyone to pay back their loans plus the interest on those loans. Without such growth, there is insufficient money to pay back loans plus interest, and a negative feedback loops ensues: some people and companies can’t pay back their loans, so they default, and the money they owe literally disappears from the ledger of their lender. If they are companies, their employees lose their jobs, so the households of those employees spend less money, putting pressure on other businesses because of lost sales, leading to more layoffs and more defaults. Many who have lost their jobs are unable to pay their mortgages and the price of real estate, which is the collateral for Trillions of US Dollars in loans, decreases. It’s a vicious feedback loop, an economy in reverse, an economy that is shrinking, deflating. To defeat this deflationary trap, governments resort to lowering interest rates to ease the debt burden, and if that doesn’t work, they print money to try to replace the money that disappears when debtors default.

These strategies supporting growth are accepted by most, even some who realize that these financial tactics are unsustainable and will possibly lead to economic calamities such as governments defaulting on their debts and/or hyperinflation.

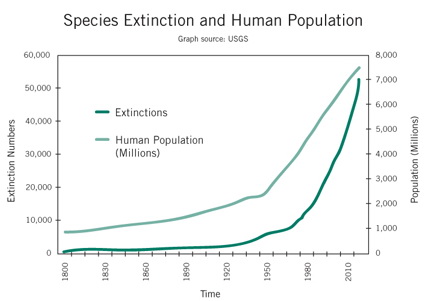

This growth-at-any-cost mentality, this quest for infinite growth, is now embedded in the system, but it conflicts with the finite resource base currently needed to enable such infinite growth, over-taxing supplies of natural resources and causing widespread environmental destruction. In our current state of human and technological development, growing economies need increasing amounts of oil, coal, natural gas, and uranium for energy; cement, copper, and lumber for construction; iron ore, steel, and a wide array of metals and chemicals for manufacturing; and fertilizers and pesticides for more food for an increasing population with increasing amounts of money to spend. Thus our often-rapacious quest–for raw materials, farmland, wildlife on land and in the sea; increasing space for housing; and the rampant use of herbicides and insecticides–robs the natural world of habitat and life, and increasingly poisons water, land, and air. Thus humanity is now the primary cause of what is shaping up as the sixth great species-extinction event in the multi-billion year history of our planet.

Some scientists think it so likely that we will destroy our own habitat, and thus our own species on Earth, that they are dedicating their life to finding other planets that could support human habitation, and devising ways to transport us there—typically only some of us.

If all money were not debt, with the ever-present pressure to pay back a loan plus interest, there would be no need for this growth-at-any-cost mentality. Economies could achieve relative stasis. As with all processes in the physical plane, the economy would be very likely to have a natural cyclical ebb and flow. And yes, some people would still seek growth, but it would not be a structural necessity of the system, that is, there would be no financial danger to the system if the economy failed to grow at all times. Thus this financial system based on money as debt is inherently unstable, and dangerous to many species, including our own.

Legal Tender Laws

The legal tender laws of nations serve to solidify the structural grip that debt-based money holds on the populace. These seemingly innocuous laws state, in the United States, for example, “United States coins and currency…are legal tender for all debts, public charges, taxes, and dues.” This means that anyone can tender (offer, that is) US Dollars to discharge any debt in the US. Any court of law considers such an offer sufficient to discharge the debt.

And while the US claims it does not force people to use US Dollars, the effect of legal tender laws is nearly that in most cases. Let’s say you lend someone 5 ounces of gold for a year at 5% interest. At the time of the loan, the gold was priced at $1,000 per ounce. So at the end of the year, you would be owed $5,000 plus 5% interest, for a total of $5,250. In the US, after a year, the borrower could offer to discharge his or her debt for $5,250 in US Dollars even if the price of gold had doubled. This has the intended effect of making sure that people not use gold in their borrowing and lending, but use US Dollars instead.

Secondly, despite the huge moves in the relative prices of currencies today (for example, the Euro declined 25% in price versus the US Dollar from March 2014 to March 2015), the legal tender currency is assumed to have a constant value so there is no additional income tax required when someone accumulates their national currency in the year 2000 and spends it in 2015. But if a person acquires a gold or silver coin, a foreign currency, or a bitcoin or other cryptocurrency, in the year 2000 and spends it in 2015, then this is a taxable event for income tax purposes, often at both the national and provincial/state level. The tax authorities consider accumulating and spending something other than the legal tender currency to be the acquisition and sale of an asset, and they require that people report it as such on their tax forms.

So yes, if you buy a bitcoin in January and buy a cup of coffee with a portion of that bitcoin in February, some countries require that this be reported on one’s income tax form. They want to know if you acquired that bitcoin at a lower price than it had when you spent it, in which case you owe taxes on the gain in value of that bitcoin. Certainly the same is true for the use of gold, silver, or platinum coins. Such laws are an intentionally strong discouragement against the use of anything other than the legal tender currency issued by the government. Perhaps even more importantly, these laws discourage transactions that take place outside of the banking system since the banks cannot take their cut from transactions that take place outside of their system.

So while countries typically claim they do not force the use of their currency, there are strong penalties for not using it, and thus gold and silver coins remain in vaults, in hiding, and do not typically compete with government fiat currency for transactions.

Governments do not want other currencies competing against their officially-sanctioned fiat currency because this would limit their ability to manipulate that currency at will, which typically means the creation of more of that currency than is prudent. Even though many become aware that their currency is losing value due to its debasement via over-printing, legal tender laws provide a level of entrapment in the government currency regime. If people start using the currency of another nation or precious metals for transactions, this weakens the hold of the government/banking cartel that gains great advantage, as shown above, over all others by being the sole controllers of currency creation.

When legal tender laws fail to stem the tide of abandonment of a national currency due to its over-creation or due to fear that its banking system is collapsing, governments will typically impose capital controls that prohibit the movement of currency out of the country and sometimes make it illegal to convert money into or use other currencies or precious metals. When announced, these measures are generally said to be temporary, but they often become permanent.

Government Guarantees for Banks; Derivatives

When people buy a product or service, they generally care about the quality of the vendor from whom they are buying. They want to buy from someone who stands behind their products and offers some level of quality guarantee, and who will remain in business to back that guarantee.

However, there is, again, a single business for which this is not the case: banks. Most people bank where it is most convenient for them based on the location of bank branches. Few take any interest in whether the bank is operating in a sound financial manner because they believe their deposits are covered by a government guarantee. So if the bank goes bankrupt, government deposit insurance will give them their money back.

The banks claim this is fair because, in many countries, they pay money into an insurance fund that backs people’s deposits. But these insurance funds typically have less than 1% of the deposits they are insuring. When there is a crisis of confidence in banks, that less-than-1% isn’t remotely enough to cover deposits of failing banks. But as shown during the phase of the financial crisis in 2008-2009, governments go far beyond these bank deposit insurance funds to protect banks, calling them too big to fail, and thus, money is borrowed or printed to keep the banks afloat.

This unique arrangement for banks allows them to engage in highly risky financial maneuvers that are unavailable to others. The most egregious area for this type of behavior is in what are called derivatives. These complex contracts provide insurance against—and allow people to gamble on for potential profit–nearly every conceivable movement of interest rates, currencies, stocks, commodities, and so forth. But because of this unique government backing, banks are allowed to sell this wide-ranging insurance with nowhere near the reserves that would be required were a regulated insurance company to sell the same coverage. Banks even sell insurance against governments going bankrupt, including their own, even though their ability to make good on such contracts could only possibly come from the government whose debts they pretend to be insuring. To give just a hint of the size of the risk involved with these derivatives, the largest US and European banks have risk exposure to derivatives of hundreds of Trillions of US Dollars, almost ten times the size of the entire world economy.

Selling these derivatives is extremely profitable for the banks, so these absurd levels of risk are tolerated and excused away. Many derivatives are, in fact, a blatant form of fraud since seller could not possibly make good on these contracts. But since it is bankers who in fact write the laws for these contracts, it is all “legal.” While things are going well for the banks selling these contracts, they pull in staggering profits from this activity. When these bets go wrong, the burden of the losses is placed on the taxpayer.

To give an idea of this in numbers, as an example, at the end of 2014 in the US, the bank deposit insurance fund held $52 Billion, insuring $6,200 Billion in deposits (119 times the insurance fund), and backing $239,000 Billion In derivatives (4,596 times the insurance fund).

In addition, it is the trade in derivatives that now move prices in global markets for many commodities, including essentials such as oil, wheat, and corn. The value of trade in derivatives for a commodity can be 100 times larger than the value of trade in the actual commodity. Thus prices are often set through derivatives, not through trade of the actual physical commodity, allowing prices to be moved far from the fundamental value of the commodity, and offering opportunities for outsized profits from magnified price movements that can have severe negative effects on the producers and consumers of essential goods.

Furthermore, many derivative trades are private transactions between parties, often defined by complex contracts that are hundreds or even thousands of pages in length. Efforts to bring all of these trades into the clear light of day on public trading exchanges have been successfully resisted by the large banks, offering the potential for illegal manipulation of markets, yet another potential source of outsized profits.

Financial Domination of Politics

Increasingly, because of the need for massive campaign funds in modern electoral politics, the political class is beholden to those who provide what are politely called “donations” or “contributions” to campaign coffers, but which have become difficult to distinguish from bribes.

Increasingly, national and major state/provincial electoral politics looks like this: prospective candidates meet with extremely rich potential contributors to secure startup campaign funds and the funding promises needed to mount a full campaign. It is at this step that candidates are actually selected—often by billionaires. After this step, actual campaigns are carried forward, first among entrenched party operatives, and finally the campaign is brought to the public where many if not most people often feel like their vote–if they bother to cast it at all–is being cast for the “lesser of two evils” or for “the devil we know versus the devil we don’t.”

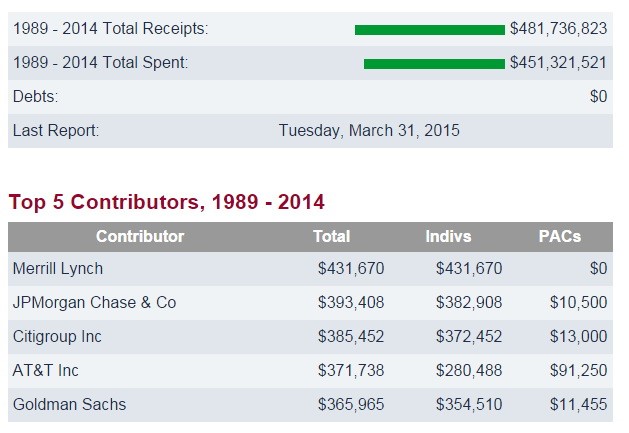

As an example, here is the fundraising and spending from 1989 to 2014 of a single US Senator, John McCain:

So, over the last 25 years, Senator McCain raised and spent almost a half billion US Dollars on his campaigns. And four of his five largest donors are from Wall Street. What are the odds, when any matter relevant to banking or markets arises, that McCain would listen to concerns of you or me, or even a large group of us, versus the concerns of Merrill Lynch, JP Morgan, Citigroup, and Goldman Sachs?

This close connection with contributors increasingly extinguishes differences, once in office, of the actions of the various political parties, regardless of pre-election campaign rhetoric. In other words, once in office, this political class, regardless of party affiliation, enhances the positions of those already in charge of the status quo in almost every respect because all too often, it is doing the bidding of its donors, who often provide major funding to all prominent political parties. If a prominent member of a political party challenges a funding industry, that industry will threaten the entire party with denial of funds:

Thus, substantial portions of the huge flow of tax money discussed above are not used to serve the people but to increase the profits of those sectors of the economy that already have sufficient funds to be among the largest of campaign donors, seriously widening wealth inequality in the society and, in effect, taking from those who have less for the benefit of those who already have much more, enabling the very rich to purchase even more political influence and to further entrench the existing political elite. Some label this “crony capitalism,” but it is not capitalism at all, it is theft and oppression by a small, oligarchic class that has learned how to manipulate the system for the personal gain of a small group.

The Revolving Door: This stranglehold on government by big-money interests is further cemented by what is called the revolving door policy. This is the movement of personnel between roles as legislators and regulators and the industries supposedly subject to the legislation and regulation. The excuse for this policy is that industries are now too complex to be regulated by those who are not industry insiders. This enables members of an industry to write, approve as law, and enforce the legislation and regulations that are supposed to assure the fair play of those industries within the society but which instead guarantee substantive advantages and large financial flows to these industries.

Conclusion

Is this picture becoming clear? We have structures in the world where:

Banks (commercial and central) can create money with zero effort while the rest must work for it, often with great effort;

People are laboring under a tremendous burden of income, sales, property, and utility taxes and fees that can take 50% or more of their income; much of this tax money flows to those who have the means to strongly influence, if not outright control, government actions to assure that even more of that tax money flows in their direction;

Debt has become so integral in government, business, and personal financing, and in the creation of all products and infrastructure, that 30% of the price of almost all products is due to interest expenses in the supply chain; if people take on personal debt in the form of mortgages, car and student loans, or credit card debt, then their personal interest expense burden is even higher; this leads to a massive flow in interest payments paid by everyone but concentrating in the hands of a small group who use that money to buy up large portions of the productive resources of the planet;

Any money saved constantly loses purchasing power by design, pressuring people to spend, borrow, and to put their savings into risky assets;

When all money is loaned into existence, it forces organizations into a growth-at-any-cost mentality that threatens crucial natural systems that support our life;

People are born owing a substantial sum of money that is part of an ever-growing national debt that can never be fully repaid.

Ideas to undo structural unfairness are rarely even part of the political debate, and if they do surface in public, are quickly squashed by the entrenched political and financial elites.

Is it any wonder that the vast majority of people on this planet are struggling financially? They are placed under a tremendous burden of debt and taxation from the moment they are born, and any money they save inexorably loses purchasing power.

The overall effect on people is twofold:

First, if an economy based in fairness can rightly be called the voluntary exchange of service for service among people, what people see is that some players in the economy receive a service without rendering one in return. They see that some of these players become vastly rich in the process and that they then strongly influence the political process to tilt the entire economic table even further in their direction. With such examples on full display, more and more people focus their efforts on getting something for nothing, on gaming the system rather than producing real value that they can rightfully exchange with others in the marketplace. People with money increasingly focus on making money from their money in the world’s giant financial casinos through stocks, bonds, currencies, commodities, futures, options, cryptocurrencies, and so forth. They don’t see debt as a burden that depresses future expenditures, they see it as a way to get rich from other people’s money, and seek to qualify for as much debt as possible. A home is no longer primarily a place in which to live, it is now an asset class to be re-modeled for resale value, flipped, and borrowed against to meet expenses or to make even more money in other asset classes. People along the entire financial spectrum seek handouts from government programs and jump through hoops, sometimes less-than-legal hoops, to avoid taxes. People see the richest using tax loopholes to pay a smaller percentage of their income in taxes than a typical worker. People see that those with money can bully the courts and regulatory systems into allowing them to get away with illegal actions—perhaps, for truly egregious actions, they receive a fine that is small compared with the profits earned from outright illegal activity–and thus clever lying becomes honored in the society.

In a society where the money is created from nothing by a small group, getting money for nothing, generally through tricks and sometimes by lying, becomes the focus of more and more people. The economy becomes an increasingly hollow competitive shell of money chasing money wherein there are always “winners and losers” rather than a vibrant, productive joint effort based on a cooperative win/win approach for all.

Second, when all money is loaned into existence and thus all money is debt, and interest must always be paid on that money, there is always a general feeling of not having enough, or a fear of perhaps not having enough right around the corner. Everyone falls in with the environment-endangering growth-at-any-cost mentality since standing still economically does not feel like a valid option to people when interest must always be paid, the paper/electronic currency constantly loses purchasing power, and taxes must be paid at every turn. This gives rise to a feeling of scarcity in a world awash in abundance and leads to the feeling that people must compete with others for scarce resources or they will die starving and penniless in the street.

IT DOES NOT HAVE TO BE THIS WAY! This is a set of structures intentionally designed by a small group of insatiably greedy conscienceless people using us and nature as cannon fodder and who have commandeered academia and the mass media to convince us that it must be this way, that in fact this way is glorious. It is not. Structural unfairness is not inevitable. We have the know-how, power, ability, and to make this world a far, far better place.

* * *

Thank you for reading this series of posts on the structural unfairness of our current system. I look forward to your comments.

(Note: As explained here, this is a draft of a chapter from an upcoming book on vanquishing financial problems once and for all. Part 1 provided an overview of the structural unfairness in the system that makes extreme wealth inequality inevitable, and covered how that unfairness is implemented through money creation by banks and taxation.)

Money that is Loaned into Existence

Over the first three quarters of the 20th Century, the world’s monetary system was incrementally changed from a system where most money was either gold or silver—or was a certificate backed by one of those—to a system in which almost all money was loaned into existence by those with a government-granted license to create such money, primarily central and commercial banks. These banks do not simply create the money, they grant access to that new money by lending it. This means that, other than coinage and physical cash, which are a very small portion of the world’s money supply, all money is debt, that is, it must be paid back by the borrower with interest.

Most people do not think of their money as debt. They feel that, if they have a bank account, their money is stored in a bank. They do not think that they have loaned that money to the bank, but that is the truth. The bank now owes the person money, plus perhaps some interest on that money. Almost all accounts for which depositors receive a paper or electronic statement involve money that has been loaned to a financial institution.

This reality has created severe problems:

First, a significant portion of the price people pay for anything is interest expense. Let’s say a person buys a bicycle. Many businesses were involved in creating that bicycle. A bulk shipping company transports iron ore from a mining company to a steel mill that supplies steel to a bicycle company that shapes the steel and then paints it with paint from a paint company that has its own suppliers of raw materials from which it makes the paint. Another shipper ships rubber from a plantation to a company that makes the tires and a trucking company hauls the tires to the bicycle plant. The finished bicycle, with many parts attached and provided by yet another set of companies, is shipped to a wholesaler who ships it to a retailer. Each of these many companies is using energy in the form of transport fuels and electricity supplied by an energy company that also has its suppliers of raw materials that were mined, shipped, and so forth.

Most or all of these participating businesses are likely to have loans on which they pay interest. People who have studied this process, such as Monneta.org, say that on average, 30% of the price of any consumer product is due to interest payments made all along the supply chain.

Furthermore, all of those businesses used infrastructure such as roads, bridges, and port facilities built by government projects that are often financed by bonds, that is, by borrowing by the government. Monneta.org has studied this process and determined that the cost of government infrastructure projects would be cut by 40% if there were no interest to be paid on the funds for the project. Thus, much of what people pay in taxes goes to cover interest expense.

This 30% of every consumer product and 40% of every government infrastructure project for interest payments are a massive burden on people, on the society as a whole. (Add this interest payment burden to people’s tax burden and it is no wonder that so many people are struggling financially!)

Next, if everyone is paying so much interest, who is collecting all that money? Who benefits? Clearly, the lenders, that is, banks and those with sufficient means to lend money. Monneta.org takes its statistical analysis of this interest expense phenomena further and shows that 60% of all interest payments concentrate in the accounts of 10% of the populace. They show that the worst of the burden falls on the middle class, which pays a lot of the interest flow on purchased products and through taxes and yet collects relatively little of the interest flow compared with the wealthiest 10% of the population.

Monneta.org has a clear, concise 7-minute video on this topic called A flaw in the monetary system? about interest expenses, the concentration of wealth, and the gargantuan expansion of financial assets entirely out of proportion with the real economy:

Thus we see another major structural unfairness built into the system: money loaned into existence burdens the entire society for the benefit of those who can create money from nothing and those with the greatest amount of money to lend.

Money Designed to Lose Purchasing Power

As we have seen, when money is loaned into existence, there must always be more of it in circulation to pay back the principal plus the interest on the loan. Thus, central banks see it as part of their task to make sure that the supply of money in the society is ever growing to support an ever-growing economy. They publicly state their goal of keeping inflation in the general level of prices at 2% or 3% per year and they do their best to make sure that enough new money gets created to support that increase in prices. They do this to avoid the dreaded-by-them deflation during which there is a more or less widespread difficulty in the repayment of loans plus interest and, instead of money getting created and increasing, loan defaults lead to money simply disappearing from the ledgers of lenders, so the supply of money shrinks. During such periods, the central banks work even harder to make sure that new money gets created. Thus, they seek to have money creation occurring in both good economic times and bad.

But what is the effect on people of having the general level of prices increase 2% to 3% per year? To put it in Dollars, in the US, during a period that the authorities say is a period of relatively low inflation of prices, it takes a $1.46 in 2015 to buy what a person could buy for $1.00 in the year 2000. And this is using US government statistics that are designed to understate inflation, so the truth is very likely worse than that.

What is the effect of this inflation on people? First, it discourages saving and encourages spending. Many realize that if they simply save money, that this price inflation inexorably erodes the purchasing power of their savings. Second, it encourages accumulation of debt. People realize that they can get a loan now and pay it back later with cheapened money. Third, it pressures people to put their money into investments or speculations that they hope will provide a return that is greater than general price inflation. Thus they enter the world of risk assets: speculation in stocks, bonds, currencies, commodities, real estate, and so forth.

This is where the problem of dishonest money arises. Some call for a return to honest money, and by this they generally mean money that is gold or silver, or is backed by one of those. People generally understand that money is useful because it is a medium of exchange and a store of value. The dishonest part arises because of this inexorable loss of purchasing power due to intentional inflation. This puts the honesty of the store of value aspect of paper/electronic money in question because, in the long run, paper/electronic currency is a very poor store of value. In addition, historically, almost all such currencies have lost all of their value, disappearing entirely or being replaced by a new version of the currency that removes a few zeroes from the old currency, that is, 1,000 of the old currency is replaced by 1 of the new currency.

Perhaps the best definition of honest money is money that does not purport to be something that it is not. (For a discussion, see this.) Paper money that is not backed by anything tangible has proven to be an excellent medium of exchange, but a very poor store of value. This will be discussed in more detail in a future post. For our purposes here, what we see is a structure that encourages people to spend now and discourages the independence and security brought about by a person having some savings; that encourages them to take on debt that creates more interest payment flows for lenders; and that encourages entry into financial speculation that inevitably enriches the Wall Streets of the world.

Photo source: @wmiddelkoop

Government Borrowing

The once flourishing and powerful Mesopotamian, Roman and Bourbon dynasties, as well as the British empire, ultimately lost their great economic vigor due to the inability to prosper under crushing debt levels.

—Van R. Hoisington and Lacy H. Hunt summarizing works by David Hume and Niall Ferguson

Most governments around the world are in a simple and intractable predicament: they have made promises they can’t keep, they continually borrow more money to try to meet those promises, and if they break those promises, they are thrown out of power.

Let’s say a government decides it needs a fire department and that their budget allows them to hire 15 firefighters. Part of the compensation for these firefighters is the promise of a pension and healthcare for their retirement years. When these 15 firefighters retire, of course a few will die, but let’s say that 12 of them collect their pension for many years. Now the city must hire 15 new firefighters and they are paying 27 firefighters instead of 15. People live much longer now. With retirement cycles, they may end up paying 30 or more firefighters, some active, some retired, with pensions indexed to cost-of-living increases and with the price of healthcare benefits accelerating faster than the government’s tax receipts for all 30 of the firefighters and their families. So the current cost for firefighters now dwarfs that original budget. It has likely increased several-fold.

Now, add to this small example soldiers, police, school teachers, garbage collectors, administrators, tax collectors, secretaries, spies, building inspectors, diplomats, jailers, judges, clerks, elected officials, border guards, road builders, attorneys, programmers, researchers…you get the picture.

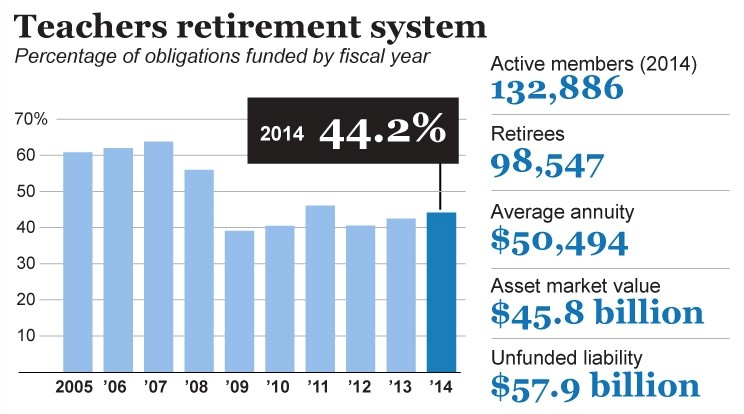

Here is a chart from the Wall Street Journal demonstrating this pension problem from just one of the states of the USA, and just for schoolteachers:

This state has 132,866 active teachers and 98,547 retired teachers. They have assets of $45.8 billion to meet retirement payments, but that is only 44% of what they really need, that is, they are $57.9 billion short. This is called the unfunded liability, that is, promises have been made but they do not have sufficient money to meet those promises. This example, from just one of fifty US states and just for school teachers, gives an indication of the magnitude of the pension shortfall faced globally by governments.

Some say that a key factor in the demise of the Roman Empire was pension promises to soldiers: things worked well while military campaigns brought home the plunder of war, but when the flow of plunder subsided and the number of pensioner-soldiers increased, the massive amounts owed led to payment in severely debased Roman coinage, where base metals were substituted for precious metals, the money-printing technique of those times. To keep their pension payments coming, Roman soldiers sometimes sacked a city to make their point.

It is essential to understand the nature of borrowing: it pulls forward future spending into the present. It allows a person to buy now something for which they have not yet earned the money. But the need to pay that bill in the future, when the money is finally earned, often depresses future spending. When a person has debts, there is usually a payment due every month that is added to the burden of their current expenses. As debt builds up, the person might not be able to spend as much as they wish on current needs and wants. When debt builds up for a society, it can have an increasingly depressing effect on the entire economy. Too much money has to be spent to pay for expenditures from years ago. We are all observing this now across most of the world, with economies groaning under their massive debt burdens.

While government borrowing began to support war and still does, currently it is often justified like this: “We will borrow money now to pay for infrastructure—roads, bridges, and schools, for example—that will be a benefit over decades. By borrowing to pay the cost over 30 years, we spread that cost to the many taxpayers who will benefit from these investments over those next 30 years.” While this has some logic to it, the reality is that infrastructure spending is now only a small portion of the spending of most governments. Most government borrowing now supports current consumption and huge standing bureaucracies.

This distinction is crucial. When a business borrows money to buy equipment that it can use to increase production, then the plan is that the use of that equipment increases company income so that paying the loan plus interest is easy, hopefully with more money left over for profits. Most consider this to be productive debt. But if that same business borrows money to pay rent, utilities, and salaries, how does that present spending produce the future income needed to repay the debt? The same applies to individuals. Financing a car can make sense for people: perhaps it allows them to travel to their job where future income will pay the auto loan plus interest. But when they are borrowing for current rent, food, utilities, vacations, and so forth, the debt tends to build up and, in the future, they must add the cost of paying the debt to then-current costs for rent, food, and utilities.

Borrowing for current consumption, except to cover an emergency that can easily be determined as short-term in nature, is a losing game. The debt for today’s expenses piles up as more debt is added for tomorrow’s expenses. When the amount of debt and interest payments overwhelm the borrower, they are bankrupt, that is, there is no way they can pay back their loans.

Most world governments are in this situation today. Their debt load from the past pressures their ability to spend in the present. And there is no conceivable way they can repay their debts. Yet people keep loaning them money as if nations never go bankrupt, never default on their debt. Here is a chart from The Economist showing country debt defaults from 1800 through 2014. And this chart only shows those countries that have defaulted at least four times, the rest are not shown. Note that the list includes supposed financial stalwarts like Germany:

When countries are unable to repay their loans, it is often a disaster for the regular people of the country. Rich people typically have ways to relocate and shelter their resources, but these methods are unavailable or unknown to the middle and lower financial classes. Essential products and services often become unavailable, leading to hunger and severe medical problems. People’s life savings are often wiped out by bank collapses and/or currency collapses in which multiple zeroes are lopped off the old currency as it is replaced with a new currency. The suffering in recent years of people in Argentina and Greece demonstrates these problems.

Countries are borrowing with no intention to fully repay the loans. We see overly-indebted countries struggling to create inflation so that they can repay current loans in future currency that is far less valuable, in other words, they borrow today and hope to pay the loans back in cheapened currency.

Countries are saying to their children and unborn citizens: we want our benefits now and we want you to pay for them. People who claim to want to create a great legacy and life for their children and grandchildren think nothing of lobbying the government to keep and increase their personal benefits which that government clearly cannot afford. Spain, Austria, France, Japan, the UK, Canada, and the Czech Republic have all sold 50-year bonds. Mexico has sold 100-year bonds. These bonds finance current consumption and the taxpayers 50 to 100 years in the future are expected to pay for that current consumption.

As if the preceding sins are not enough, perhaps the greatest immorality is the one that is hidden from most people: interest payments on all this debt go mainly to those who are already financially secure, paid for by those who are much less so. Monneta.org has shown only those who are financially in the top 10% are net beneficiaries (they receive more interest payments than they pay out in interest and taxes) from all this interest expense. And the amounts of interest are huge. From 1988 through 2014, the US federal government, for example, has paid $9.4 Trillion in interest. With the current national debt at $18 Trillion (in early 2015), clearly a huge portion of the accumulated national debt is due to interest payments. Since the few benefit from these interest payments as the rest of the populace pays the bill, once again we see the intentional structural unfairness that pervades the entire financial system.

Governments borrowing money into existence

Almost every government today does not simply have its Treasury Department or Finance Ministry create its national currency, it grants that concession to its central bank, which lends that money to banks or the government itself. Thus, as with commercial banks, the money is loaned into existence and interest must be paid. In some nations, the central bank is a branch of the government, in others it is a private bank. Either way, the money is loaned into existence, saddling the entire society with massive debt that requires interest payments. Were the government to either back its money with gold or silver, or to simply create that money without borrowing it, the taxpayers of nations would not be saddled with today’s huge interest payment burden.

Why is it done this way? Well, what is the job of the central bank? Since it can create infinite amounts of money if needed, it is considered the lender of last resort when there is a financial panic. And whom does it save during financial panics? Primarily banks. So the real job of this central bank is to protect commercial banks, to assure that their money creation cartel remains intact.

And what is the first resort when a nation gets into trouble because its debt load has become too large? More loans! This is always the solution from international banking organizations such as the International Monetary Fund. So the fire of too much debt is fought with additional fire, placing an even larger debt burden on the already over-burdened taxpayers of a country, who now owe even more money to bankers. If an economically-troubled nation does not cooperate with these measures to saddle them with even more debt, the international banking community threatens them with various types of monetary exile—such as lack of access to markets to export their own products or to import essential products not produced in that country—that will turn their economic situation from a serious problem into a humanitarian disaster.

In this manner, all nations and their people become debt slaves. This is a key element in the very well-devised plan for structural unfairness in the financial system.

(Note: As explained here, this is a draft of a chapter in an upcoming book on vanquishing financial problems once and for all.)

AVOIDING STRUCTURAL UNFAIRNESS

In a condition of societal financial collapse, and its associated privations, people are understandably desperate to reinstate that which prevailed before the collapse. This is a poor choice when that which is familiar is inherently flawed in ways that:

made financial collapse inevitable and,

caused a great deal of unnecessary pain prior to the collapse due to structural unfairness in the financial system.

Thus, to avoid creating a future that necessarily includes the pains resulting from structural unfairness (among people, businesses, and regions) and inevitable financial collapse, it is crucial that we all understand the preventable flaws of the modern financial system to assure that these flaws are not reinstated. Repeating these flaws guarantees a world where a very few have great wealth, where a very large number of people struggle daily for basic necessities, and where the vast majority works daily to provide more for the very wealthy few.

The Problem: Structural Unfairness, an Executive Summary

It is essential that people understand this concept of structural unfairness. Allowing structural unfairness means there is no “level playing field” for all parties. It guarantees ever-growing and societally destructive wealth inequality. This is not wealth inequality based on inevitable differences in financial effort and talent among people, this is severe inequality that is built into the system. That is what is meant by structural.

Here are some conclusions to this section, to be followed by the supporting details:

Most people and industries work diligently to produce a product or service from which they earn money. Yet one industry, banking, can create money from nothing, lend that money to others, and charge interest on that new money. It is virtually guaranteed that this single industry with access to free money will come to dominate the economic and political worlds.

Many people in the world work hard to obtain what is considered a good salary, a steady income. But when they achieve that goal in developed economies, between national, state/provincial, county, and municipal taxes on their income; VAT, sales, and fuel taxes on their purchases; property taxes; and agency taxes and fees (for example, on telecommunications and utility bills); for many, at least 50% of their income is taken.

In an economy in which most businesses in the vast supply chain that provides the world’s products and services have taken on debt in their businesses, according to those who have studied it, on average, 30% of the cost of everything people buy is due to interest expenses in the supply chain.

Because governments borrow money to fund infrastructure projects, the cost of building roads, bridges, schools, airports, stadiums, and so forth would be, on average, 40% less were it not for interest expenses on the debt for the project.

If a person in this economy takes on one or more forms of personal debt–mortgage, car loan, student loan, credit card debt, and so forth—yet another substantial chunk of their income is consumed by interest payments.

Because almost all governments have made promises they cannot keep and which are not sufficiently funded by taxes, they borrow ever-increasing amounts of money. From 1988 through 2014, the US federal government, for example, paid US$9.4 Trillion in interest on its borrowings, so a substantial portion of the US$18 Trillion national debt (in early 2015) is due to accumulated interest payments. Furthermore, these vast and accumulating government debts mean that all children are now born with a portion of the nation’s debt burden they are expected to pay so that the lenders can continue collecting interest payments; in the US as of early 2015, each child is born with a national debt burden of more than US$57,000.

Who collects these vast flows of interest payments? Those who can create money from nothing, that is, the banks; and those who have excess assets to lend. According to those who have studied it, 60% of the massive flow of global interest payments go to the wealthiest 10% of the populace. And we all now know from more detailed studies that these massive money flows concentrate further within that 10%, especially to the 0.01%, who then use those money flows to have a major influence on government and media, thus controlling the laws under which people live and the messages with which they are constantly bombarded by television, radio, and in print.

High taxation and heavy government borrowing go hand-in-hand with massive expenditures by government. Those businesses that continuously benefit from these expenditures use profits to influence elections, elected officials, appointments at regulatory agencies, the writing of laws, and media coverage of issues, continually increasing the flow of government expenditures in their direction at the expense of taxpayers and the rest of the business community. Thus, the banking cartel, the military-industrial complex, the medical-industrial complex, and so forth, become permanent, major fixtures in government budgets, strong voices always moving policy in a direction favorable to their business prospects.

The fact that all money is now loaned into existence by either a commercial or central bank means that all money is debt that carries an interest payment that must be made. This means the economy must always grow so that the loans plus interest can be paid. When the economy stays stable or shrinks, some are unable to pay their loans plus interest and money starts to disappear from the ledgers of the lenders, leading to the banker-dreaded “deflation.” Because of this debt-based money, our economies are inherently unstable and thus we hear the endless chants for “growth, growth, growth.” But what is the impact of this quest for infinite growth when our economies are powered by finite resources such as fossil fuels, iron ore, cement, fertilizers for industrial agriculture, and so forth? As we watch our growth-at-any-cost approach accelerate the extinction of species around us—many of whom provide crucial support for humanity—how long will it be before we threaten our own species?

If a person tries to save money to gain independence from this structural treadmill, their savings constantly lose purchasing power by design, pressuring them to spend, borrow (which they can pay back later with cheapened money), and to put their savings into riskier assets “to keep up with inflation.”

If a person or group attempts to operate financially outside of this web of debt, they are punished by legal tender laws that, while appearing innocuous, go a long way toward locking them into the system. The legal tender laws say that any debt can be satisfied by payment in the legal tender currency. If a person tries to operate using gold or silver or bitcoins, these forms of money are considered by the system not as legal tender, but as assets. Thus, when they are sold–for example, if you buy a cup of coffee using a fraction of a bitcoin or a barter currency—this is the sale of an asset and thus some governments want to know whether that bitcoin gained in price from the time you purchased the bitcoin to the time you “sold” it to buy coffee. And they want to tax you on any gain. Thus, alternatives to the government fiat currency such as gold and silver go into hiding in vaults as forms of savings and are not used for transactions.

Attempts to undo structural unfairness rarely surface as part of the political debate, and if they do, it is the voices of those providing the bulk of financing for expensive modern political campaigns that are heard and heeded, increasing structural unfairness rather than undoing it.

While this is not the complete picture of the structural unfairness in our current system, let’s take a quick look at the finances of someone who is “doing well” according to the world, that is, earning what is considered to be a very good salary. Between national, state/provincial, local, property, VAT, sales, fuel, and agency taxes and fees, at least 50% of their income is directly taken. Then, of almost everything they buy, 30% goes to interest expenses. If this person has any debt of their own—such as a mortgage, automobile or student loan, or credit card debt—then another serious portion of their income is dedicated to interest expense. Any money they save constantly loses purchasing power. Is this person really “doing well”? Or have they been enslaved by those collecting taxes and interest? If the minority on this planet that are said to be “doing well” are often in or near financial difficulty, what about the vast majority, the billions of people who do not have that “very good” salary?

Is this beginning to sound like a movie about a criminal syndicate that collects “a piece of the action” from all businesses in an area? For the “protection” of those businesses? It should: the analogy is not far-fetched. The structures described above—structures through which a portion, a “cut” is taken of nearly every transaction in the economy—are not accidental, they are intentional:

When plunder becomes a way of life for a group of men living together in society, they create for themselves in the course of time a legal system that authorizes it and a moral code that glorifies it.

—Frederic Bastiat, The Law, 1848

Structural Unfairness, the Details

In early 2015,OXFAM showed that by the end of 2015, “1% of the world’s population will own more wealth than the other 99%.” In other words, the richest 1% own half of the world’s wealth. In early 2015, just 80 people owned the same amount of wealth as the poorest 3.5 billion people on the planet. And the trend toward extreme wealth inequality is accelerating, with the wealth of those 80 people doubling between 2009 and 2014.

This is not accidental, this is by design.

The major structural problems that relentlessly add to this extreme disparity will be shown in these sections:

Money Creation by Banks

Taxation

Money that is Loaned into Existence

Money Designed to Lose Purchasing Power

Government Borrowing

Governments Borrowing Money into Existence

Growth at any Cost

Legal Tender Laws

Government Guarantees for Banks; Derivatives

Financial Domination of Politics

Money Creation by Banks

One primary source of structural unfairness is granting bankers—both commercial and central bankers—the license to create money from nothing and to charge people for the use of that money. A bank does not lend cash from its vaults, it creates ledger entries that create money.

The process by which banks create money is so simple the mind is repelled. –John Kenneth Galbraith, economist, professor—Harvard University

Commercial Banks

Let’s say you sign up for a four-year car loan from a Bank A. Bank A now claims it has an asset—your promise to repay the loan. It creates a ledger entry recording the fact that you will be repaying the loan with interest in installments over four years. So for the next four years, each month, you pay the bank a portion of the money you borrowed plus some additional money as interest, the fee the bank charges you for renting money from them. (If you don’t pay, the bank will claim your car by repossessing it.) If the car dealer is also a customer of Bank A, then the car dealer’s account is credited with the amount of the loan. That’s it. The transaction is done. The money has been created and you are charged interest over the life of the loan for the use of that money.