You know that thing about time accelerating? As of today, nearly one-fifth of 2013 is in the past!

The Age of Truth

If truth does set us free, then far greater freedom is on the way due to the accelerating emergence of truth. The controllers of the major systems on our planet react to both, that is, they react to the emerging truth by repeated attempts to squelch free expression on the internet and on the streets, and by well-funded propaganda and disinformation campaigns; and they combat emerging freedom by surveillance cameras (1.6 million in the UK alone!), repudiation of laws that protect individual freedom, complete tracking of people’s electronic activities, drone surveillance, and so forth. All under the rubrics of national security, public safety, copyright protection, and so forth. In the US, it appears that this is likely to get worse:

One problem with a discussion of the emergence of truth: On this planet, at this time, when the light of truth shines, it reveals a lot of lies. Many have come to see lies as standard operating procedure, so lies are accelerating in their frequency and boldness. This is a problem for two reasons: lies generally have consequences, victims, that is, they often do damage; and much that goes on in our world is based on trust, for example, when you buy something, you trust that it will work as advertised, and the vendor who sells it to you trusts that your form of payment has value. What is the general consequence of an increasing breakdown in trust resulting from increased lying?

Some lies are easy—once they are exposed. Horsemeat being sold as beef all over Europe comes to mind. Though this fish thing will be tougher to sort out:

New Study Shows 59% of “Tuna” Sold in the U.S. Isn’t Tuna

Other lies are more tricky because either there is a powerful constituency that supports the lie, or most people want it to be true even if it isn’t, or both. That is the category of lie described in the first major post on this site, The financial system is based on twelve promises that are lies, which described the lies at the foundation of what is called our financial system; and how the recognition of just one of those lies—the lie that real estate prices always goes up—came within hours of dissolving the world’s current financial system.

Governments lie so often now that more and more people assume that anything the government bothers to comment about in public is a lie. It would help their case if they weren’t so obvious, though sometimes one has to do at least the amount of digging that would be required on a standard reading comprehension test to uncover them.

There is a great example of a “policy lie,” and likely the often-associated “lying to keep one’s job,” at this link. It’s of interest here because we used the government’s own database to show the truth of this topic in Part 1. The post reports on a US Geological Survey study that says more people will die from earthquakes during this century than the last. But it is known from repeated examples that it is USGS policy to say that earthquakes are not increasing. So the article dutifully states that it isn’t because earthquakes are increasing that more people will die, but rather because of increasing population density in seismically vulnerable buildings. But the article blows its own policy case. They state that there were seven catastrophic earthquakes in the Twentieth Century, so that’s one every fourteen years. And then they state, and I quote: “Four catastrophic earthquakes have already struck since the beginning of the 21st century.” So that’s one every three years! So the “population density in vulnerable buildings” took a threefold leap right around the year 2000?! Nice try. This is science by policy–and keeping one’s salary or grant money flowing–rather than science by data. Such “science” is unfortunately all too common in our world.

So why does the USGS have a policy that can be easily shown to be a lie using their own database? For one, I’m sure they are correct in thinking that most people are not going to actually go look at the data, so they can say what they want about it and most people will believe it: “It’s from the government. It’s from a scientist. It must be true. What’s on TV?” For another, governments seem to think that keeping people calm is a high priority. Perhaps they correctly believe that they get to stay in power longer when the people are calm. But as each of their lies is uncovered, what they derided as “conspiracy theory” becomes conspiracy fact and they have an accelerating loss of credibility.

The same applies to billionaires. If you see or hear about them saying an investment is bad or good, assume that they are talking their book. In other words, if they say in public that some investment is fabulous, it means that they own a boatload of it and now want to get rid of it, selling it to anyone who will listen. And if they deride an investment, they are trying to knock down its price so they can buy more of it cheaper. George Soros was caught doing this with respect to gold twice in just over a year. Twice he made somewhat nebulous but definitely negative public comments about gold. In both cases, in the quarter following his comment, his hedge fund strongly increased their position in gold as its dollar price fell. These purchases are only revealed well after the fact, so they can’t be uncovered in real time. But if a billionaire bothers to hit the airwaves with investment commentary, assume that they are talking their book. One exception to this idea is Jim Rogers, but he is unusual.

Over the last six weeks, we found out more about the world’s Too Big to Jail treatment of banker crime. In the US, first the Assistant Attorney General said right on TV that he didn’t prosecute the big banks because he worried about the economic fallout:

Assistant Attorney General Admits On TV That In The US Justice Does Not Apply To The Banks

And then the Attorney General himself, Eric “Place” Holder, admitted the same in testimony before the US Congress:

Eric Holder: Some Banks Are So Large That It Is Difficult For Us To Prosecute Them

Holder: But I am concerned that the size of some of these institutions becomes so large that it does become difficult for us to prosecute them when we are hit with indications that if you do prosecute, if you do bring a criminal charge, it will have a negative impact on the national economy, perhaps even the world economy. And I think that is a function of the fact that some of these institutions have become too large.

So, big money gets a free pass from what is supposed to be the Department of Justice.

There are entire industries that live by lies:

The tobacco industry is famous for it.

The nuclear power industry, creators of vast quantities of waste that will be deadly toxic for thousands of years, has in recent years been trying to characterize itself as “green”! And there were people who are supposedly environmentalists who fell for it. It took the catastrophe at Fukushima to take at least some of the wind out of their sails.

And the oil industry is a barrel of laughs along these lines. Let’s take the case of alcohol fuel, aka ethanol. Everyone in the US now “knows”–because it was covered this way by both the liberal and the conservative press, so people think it must be true—that it takes more energy to produce ethanol than one can get from the end product. And it drives up the price of food for everyone. And it wrecks engines. So ethanol is bad.

Would it surprise you to find out that all of that “information” is vigorously and continuously disseminated by the American Petroleum Institute in a well-financed campaign to malign ethanol? That it is based on a series of studies by a single person, Cornell Professor David Pimentel (more “science”!) who is the only investigator who claims that ethanol has a negative return on energy invested and whose faulty calculations are strongly at odds with other investigators? That Brazil’s conversion from gasoline to ethanol turned the country from a struggling importer of expensive energy to a net exporter of same? That the oiligarchy regime of Bush and Cheney implemented the ethanol program in a way that was sure to make ethanol look bad? That Henry Ford wanted all cars and trucks to be powered by ethanol, not gasoline, but that a ruthless campaign by John D. Rockefeller made that impossible? Including the fact that Rockefeller funded groups who created Prohibition of alcohol as a drink in the US not because he was against people drinking alcohol but because he wanted to bankrupt the major alcohol distillers in the US (he succeeded) so he could supply oil as the transport fuel of choice? That there are farmers across the globe who distill their own ethanol on their farm and successfully run all of their machinery with it? That alcohol is clean-burning, creating no particulate pollution? So again now, what is it that we “know” about ethanol and how inferior it is to petroleum fuel? Have the engines in all of the cars in Brazil been destroyed because they are burning ethanol? It turns out that, using permaculture, it is possible to become energy independent without driving up the cost of food for anyone. In the late 1970s, PBS funded a nine-part series by David Blume on precisely how to do that. They broadcast the first two episodes. All of their oil company donors said that if they continued airing the series, those oil companies would pull all funding forever. PBS folded under the pressure, even to the point of destroying all copies of the tapes, none of which exist today.

In real estate, it’s always a good time to buy. (I was planning to do a post with that as the title, but I don’t have to, Jim Quinn of the Burning Platform did that, and he did an outstanding job):

IT’S ALWAYS THE BEST TIME TO BUY

If prices are rising, it is claimed that they will always rise forever. If prices are falling, then they said to be a great bargain. Some blogs refuse to report the exaggerations that are alleged to be statistical reports from the US National Association of Realtors. At the end of every year, the NAR quietly revises the data it reported for the past year. For several years running, they have “adjusted” the number of existing home sales down by around 800,000 per year. So they report big, increasing, “better than expected” numbers all year, only to quietly admit the truth after each year is done. (The use of “better than expected” when reporting dismal statistics in news headlines deserves a post of its own, but let’s agree to pass on that.) You’ve probably all seen the monthly headlines generated by the NAR. But have you ever seen a headline about the NAR annual revisions? Certainly not in the mainstream media.

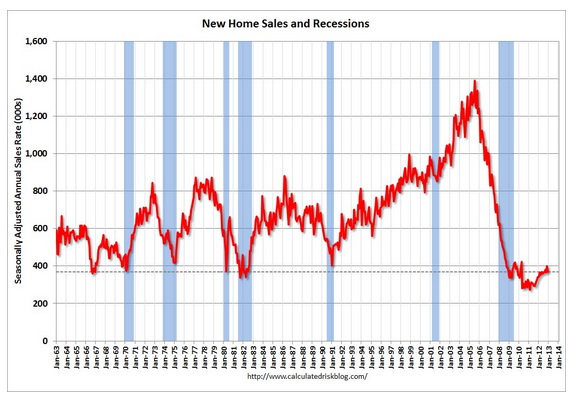

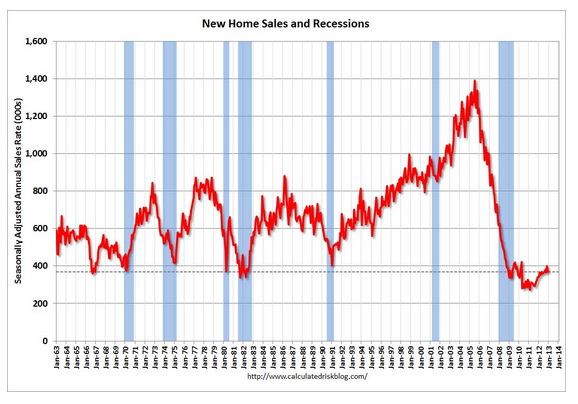

When you see some headline like “Highest New Home Sales in Three Years,” just remember this next chart. Yes, the highest level in three years. But this is a market trying to lift its face out of the mud:

Here is Jim Quinn’s comment on that chart:

The media, NAHB, and certain bloggers look at this chart and declare that new home sales are up 20% from 2011 levels. Sounds awesome. I look at this chart and note that 2011 was the lowest number of new home sales in U.S. history. I look at this chart and note that new home sales are 75% below the peak in 2005. I look at this chart and note that new home sales are lower today than at the bottom of every recession over the last fifty years. I look at this chart and note that new home sales are lower today than they were in 1963, when the population of the United States was a mere 189 million, 40% less than today’s population. Do you see any signs of a strong housing recovery in this chart?

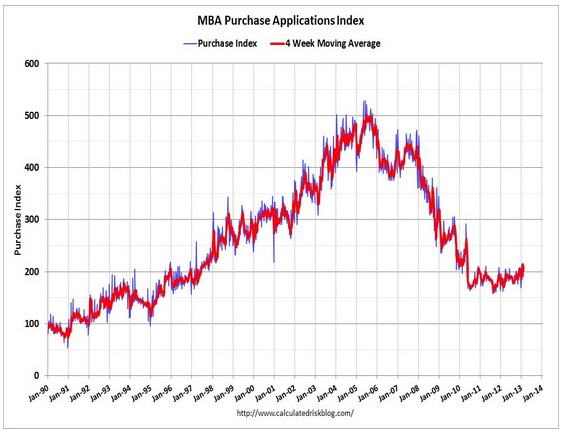

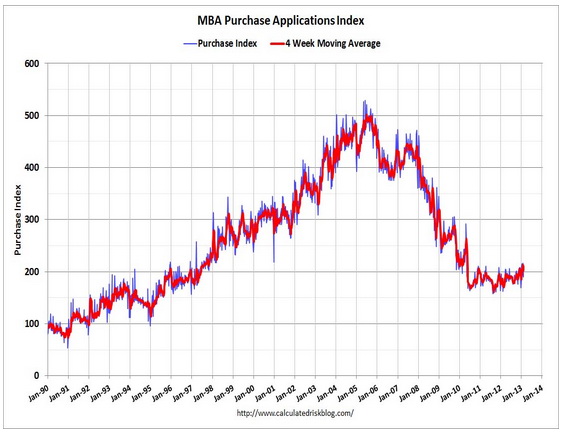

OK, when one includes existing homes sales, the picture is a little better, here’s the chart of mortgage applications for purchase of a home in the US:

So that’s back to 1997 levels. But Jim Quinn correctly notes this:

JP Morgan, Blackrock, Citi, Bank of America, and dozens of other private equity firms have partnered with Fannie Mae and Freddie Mac, using free money provided by Ben Bernanke, to create investment funds to buy up millions of distressed properties and convert them into rental properties, further reducing the inventory of homes for sale and driving prices higher. Only the connected crony capitalists on Wall Street are getting a piece of this action.

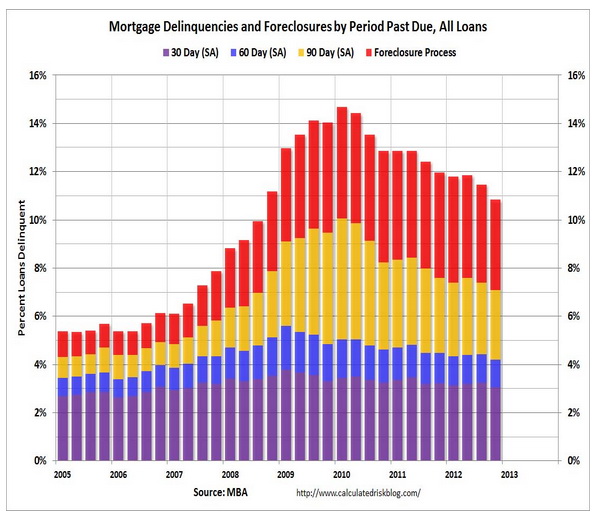

So what just happened? Through a well-orchestrated bubble followed by a continuing foreclosure fest, shown here:

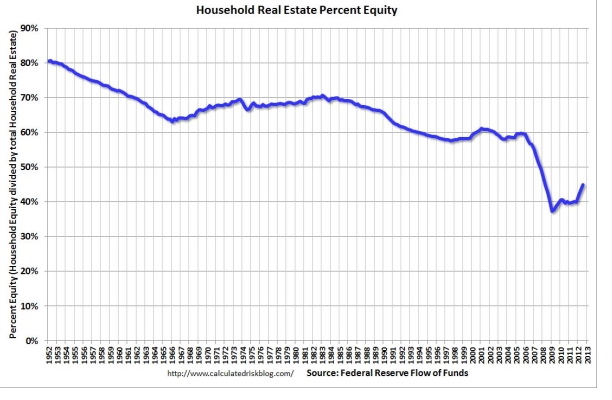

residential real estate ownership in the US is being transferred from Main St to Wall St., facilitated by free money from the US Federal Reserve. Here’s the ownership percentage of regular people in the housing stock in the US:

So that number has dropped from 80% to 43%. How does that trend look to you? Do you think all of this government real estate assistance, said to be for the benefit of regular people, is for regular people or for Wall St? And this is the system that most people hope remains intact.

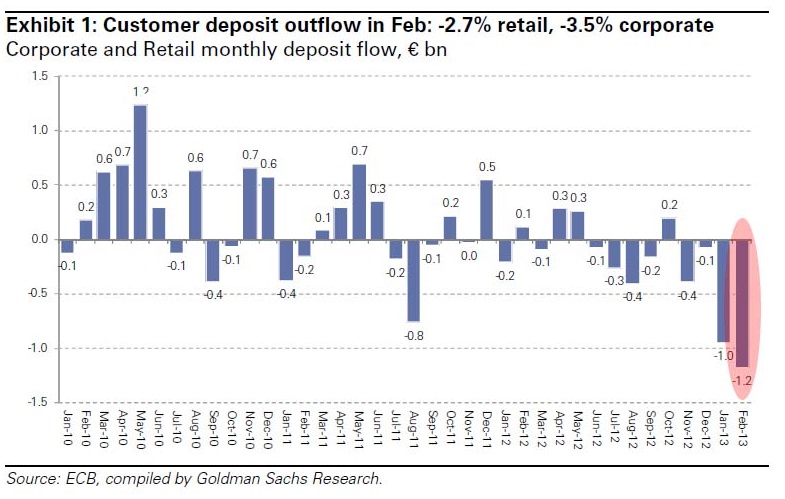

And speaking of free money from the Federal Reserve, and indeed, all central banks, the next time you see meek and mild Ben Bernanke on TV telling you he’s doing it all for you, remember who gets free money from him and who does not. The big banks get free money. You and I do not. But, if you are a citizen of the US, you might think, well at least he’s giving money to American banks. But that’s less than half true. Much of Ben’s “quantitative easing” (i.e., the fashionable cover term for money printing) has gone directly into the coffers of European banks via their American branches. Why? The US Federal Reserve is a private corporation among whose major shareholders are large European banking families. And the European banks have a lot of bad loans and their depositors are wising up and withdrawing their deposits:

Euro-Land Banks In Trouble

A recent study by Ernst & Young has revealed that euro-land banks in the aggregate now hold € 918 billion (US $1.23 trillion) in non-performing loans…

Of course we’ve all heard from the European politicians that everything has been fixed in Europe, though even a cursory look shows that to be a lie.

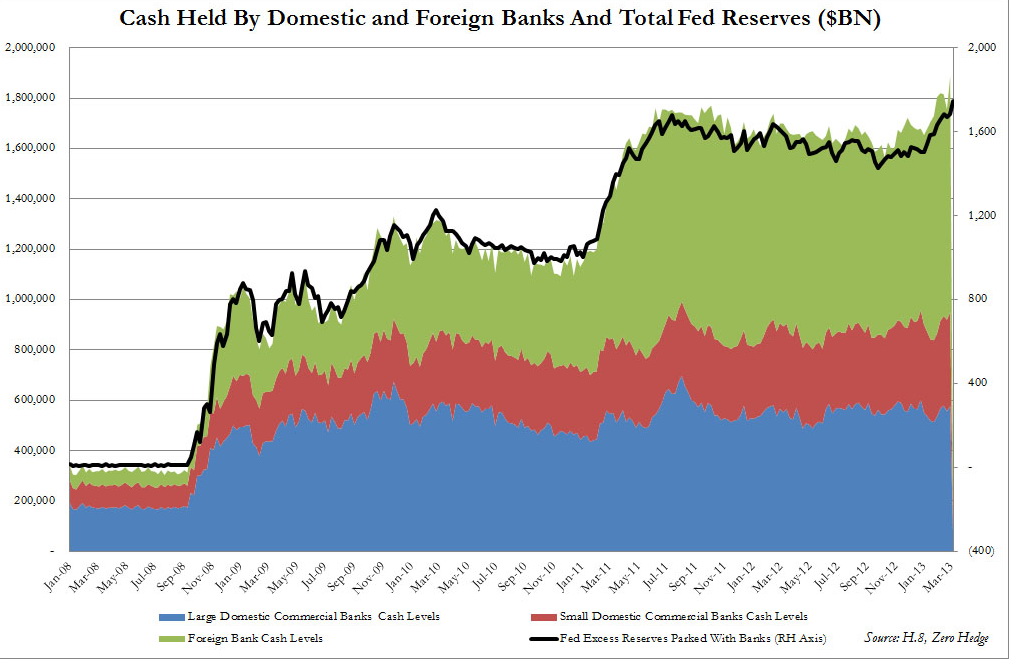

So Ben Bernanke is printing up US Dollars to bail out European banks. He testified to Congress in 2011 that he was not and would not bail out European banks. But those who track the Fed’s money printing have demonstrated that what was called QE2 (Quantitative Easing 2) did not show up on the balance sheet of US banks, it showed up on the balance sheets of the American branches of large European banks, and this has continued. The benefit to the European banks is shown here in green, correlated with the amount of money printing the Fed has done shown as the black line:

That chart is from:

Fed Injects Record $100 Billion Cash Into Foreign Banks Operating In The US In Past Week

And speaking of lying, there is a law against what the Federal Reserve is doing. The law says the Fed can’t buy Treasury Bonds directly from the US Treasury. There’s a reason for this: when the Fed prints up new money to buy US Treasury bonds, which is the borrowing of the Government of the US, it’s called “monetizing the debt,” a clear Ponzi scheme where one hand borrows and the other hand prints to enable the borrowing. There’s a law against this because many countries have gone down the tubes once they traveled that road of money printing. Their currency value ultimately went to zero. So what does the Fed do to circumvent the law? They have one of the big NY banks buy the Bonds from the Treasury and then they buy the Bonds from the big NY bank three days later. So the Fed circumvents the law and NY banks get nice commissions and the US Congress gets more free money. And your income and savings are worth less and less.

Fed Buys Back 30 Year Bond Auctioned Off Last Thursday

And the politicians and economists who support money printing claim they are Keynesians, that is, that they follow the principles of economist John Maynard Keynes. But they cherry-pick Keynes work, only using that which supports what they want to do anyway, ignoring the rest. Here is a quote from Keynes:

By a continuing process of inflation, governments can confiscate, secretly and unobserved, an important part of the wealth of their citizens. By this method they not only confiscate, but they confiscate arbitrarily; and, while the process impoverishes many, it actually enriches some. … Those to whom the system brings windfalls… become “profiteers” who are the object of the hatred…. the process of wealth-getting degenerates into a gamble and a lottery.

Lenin was certainly right. There is no subtler, no surer means of overturning the existing basis of society than to debauch the currency. The process engages all the hidden forces of economic law on the side of destruction, and does it in a manner which not one man in a million is able to diagnose.

Does that sound like someone who thought money printing was a good idea? Clearly, politicians think all this underhanded dealing is justified:

Berlusconi: “Bribes Are Necessary – They Are Not Crimes”

This section could go on for days, but let’s stop, though I would like to mention that I think it is advisable that people give consideration to those things derided by powermongers and their minions in the press as “conspiracy theory.” Many things that the mainstream attempted to relegate to this scrap heap have turned out to be true (here’s a link to an account of 33 of them).

Just one example: Many supposed conspiracies are rejected under the heading that too many people would have to know about it and that this large number of people could never keep it secret. This whole rejection methodology was blown out of the water with the LIBOR scandal where at least dozens of traders at several major banks conspired over decades to manipulate the interest rates on which trillions of dollars of contracts are based. Testimony has been given in the US and the UK that people told the central banks of their respective countries about this manipulation as early as 2008 and the central banks did worse than nothing: The Bank of England is said to have encouraged the practice. Clearly the profit motive was enough to keep this conspiracy operating and quiet for decades. So when you hear that price fixing takes place, with or without government collusion, in fossil fuels, pharmaceuticals, stocks markets, precious metals markets, and so forth, it actually appears to be irrational now to think that price fixing is not taking place. When there is big money to be made, there is big price manipulation in play. All this stuff about “free markets” is a thick, giant smokescreen designed by to increase the power of those who already have it but who crave even more.

However, between insider whistleblowers and great investigative researchers (typically outside the mainstream media that is primarily a compliant tool of those in power), using internet communication as a conduit, discovery and dissemination of truth is clearly on a meteoric rise.

This trend is strongly supported, in my view, by the accelerating increase in the number of people who recognize that individual inner work is beneficial and necessary. People who do the work to identify and become independent of lies they once blindly accepted as true, who continue working to understand the ways in which they fall for illusion, become acceleratingly tough to trick! We will take a look at this and other fabulous developments in Part 7.