(Note: As explained here, this is a draft of a chapter from an upcoming book on vanquishing financial problems once and for all. Part 1 provided an overview of the structural unfairness in the system that makes extreme wealth inequality inevitable, and covered how that unfairness is implemented through money creation by banks and taxation. Part 2 covered how money loaned into existence, money designed to lose purchasing power, government borrowing, and governments borrowing their money into existence all play their part in the structural unfairness of the system. This is the final part of the chapter.)

Growth at any Cost

A major consequence of all money being loaned into existence is the growth-at-any-cost mentality that endangers the well-being of all animals and plants on this planet. Very few nations, states, businesses, and individuals are satisfied with a steady-state financial situation. Instead, we are inundated with calls by our so-called leaders for “growth, growth, growth,” chanted like a mantra.

While there is no doubt that economic booms can make people feel good about things (and about those politicians currently in power), it is clear that governments and businesses increasingly resort to desperate tactics when growth seems insufficient and the inevitable recession or depression occurs: businesses slash their employment rolls; governments bust their budgets and borrow vast sums to fund massive “economic stimulus” programs, ignoring whether the money they borrow can ever be repaid; central banks push interest rates—the cost of borrowing (renting) money–to zero or even negative; and central banks resort to what they call quantitative easing (money printing).

The clear source of such desperation lies in the fact that money in this world is debt. If the average interest rate in the world, on all loans, is 4%, then the economy must grow sufficiently (by 4% or more) for everyone to pay back their loans plus the interest on those loans. Without such growth, there is insufficient money to pay back loans plus interest, and a negative feedback loops ensues: some people and companies can’t pay back their loans, so they default, and the money they owe literally disappears from the ledger of their lender. If they are companies, their employees lose their jobs, so the households of those employees spend less money, putting pressure on other businesses because of lost sales, leading to more layoffs and more defaults. Many who have lost their jobs are unable to pay their mortgages and the price of real estate, which is the collateral for Trillions of US Dollars in loans, decreases. It’s a vicious feedback loop, an economy in reverse, an economy that is shrinking, deflating. To defeat this deflationary trap, governments resort to lowering interest rates to ease the debt burden, and if that doesn’t work, they print money to try to replace the money that disappears when debtors default.

These strategies supporting growth are accepted by most, even some who realize that these financial tactics are unsustainable and will possibly lead to economic calamities such as governments defaulting on their debts and/or hyperinflation.

This growth-at-any-cost mentality, this quest for infinite growth, is now embedded in the system, but it conflicts with the finite resource base currently needed to enable such infinite growth, over-taxing supplies of natural resources and causing widespread environmental destruction. In our current state of human and technological development, growing economies need increasing amounts of oil, coal, natural gas, and uranium for energy; cement, copper, and lumber for construction; iron ore, steel, and a wide array of metals and chemicals for manufacturing; and fertilizers and pesticides for more food for an increasing population with increasing amounts of money to spend. Thus our often-rapacious quest–for raw materials, farmland, wildlife on land and in the sea; increasing space for housing; and the rampant use of herbicides and insecticides–robs the natural world of habitat and life, and increasingly poisons water, land, and air. Thus humanity is now the primary cause of what is shaping up as the sixth great species-extinction event in the multi-billion year history of our planet.

(Chart source.)

Some scientists think it so likely that we will destroy our own habitat, and thus our own species on Earth, that they are dedicating their life to finding other planets that could support human habitation, and devising ways to transport us there—typically only some of us.

If all money were not debt, with the ever-present pressure to pay back a loan plus interest, there would be no need for this growth-at-any-cost mentality. Economies could achieve relative stasis. As with all processes in the physical plane, the economy would be very likely to have a natural cyclical ebb and flow. And yes, some people would still seek growth, but it would not be a structural necessity of the system, that is, there would be no financial danger to the system if the economy failed to grow at all times. Thus this financial system based on money as debt is inherently unstable, and dangerous to many species, including our own.

Legal Tender Laws

The legal tender laws of nations serve to solidify the structural grip that debt-based money holds on the populace. These seemingly innocuous laws state, in the United States, for example, “United States coins and currency…are legal tender for all debts, public charges, taxes, and dues.” This means that anyone can tender (offer, that is) US Dollars to discharge any debt in the US. Any court of law considers such an offer sufficient to discharge the debt.

And while the US claims it does not force people to use US Dollars, the effect of legal tender laws is nearly that in most cases. Let’s say you lend someone 5 ounces of gold for a year at 5% interest. At the time of the loan, the gold was priced at $1,000 per ounce. So at the end of the year, you would be owed $5,000 plus 5% interest, for a total of $5,250. In the US, after a year, the borrower could offer to discharge his or her debt for $5,250 in US Dollars even if the price of gold had doubled. This has the intended effect of making sure that people not use gold in their borrowing and lending, but use US Dollars instead.

Secondly, despite the huge moves in the relative prices of currencies today (for example, the Euro declined 25% in price versus the US Dollar from March 2014 to March 2015), the legal tender currency is assumed to have a constant value so there is no additional income tax required when someone accumulates their national currency in the year 2000 and spends it in 2015. But if a person acquires a gold or silver coin, a foreign currency, or a bitcoin or other cryptocurrency, in the year 2000 and spends it in 2015, then this is a taxable event for income tax purposes, often at both the national and provincial/state level. The tax authorities consider accumulating and spending something other than the legal tender currency to be the acquisition and sale of an asset, and they require that people report it as such on their tax forms.

So yes, if you buy a bitcoin in January and buy a cup of coffee with a portion of that bitcoin in February, some countries require that this be reported on one’s income tax form. They want to know if you acquired that bitcoin at a lower price than it had when you spent it, in which case you owe taxes on the gain in value of that bitcoin. Certainly the same is true for the use of gold, silver, or platinum coins. Such laws are an intentionally strong discouragement against the use of anything other than the legal tender currency issued by the government. Perhaps even more importantly, these laws discourage transactions that take place outside of the banking system since the banks cannot take their cut from transactions that take place outside of their system.

So while countries typically claim they do not force the use of their currency, there are strong penalties for not using it, and thus gold and silver coins remain in vaults, in hiding, and do not typically compete with government fiat currency for transactions.

Governments do not want other currencies competing against their officially-sanctioned fiat currency because this would limit their ability to manipulate that currency at will, which typically means the creation of more of that currency than is prudent. Even though many become aware that their currency is losing value due to its debasement via over-printing, legal tender laws provide a level of entrapment in the government currency regime. If people start using the currency of another nation or precious metals for transactions, this weakens the hold of the government/banking cartel that gains great advantage, as shown above, over all others by being the sole controllers of currency creation.

When legal tender laws fail to stem the tide of abandonment of a national currency due to its over-creation or due to fear that its banking system is collapsing, governments will typically impose capital controls that prohibit the movement of currency out of the country and sometimes make it illegal to convert money into or use other currencies or precious metals. When announced, these measures are generally said to be temporary, but they often become permanent.

Government Guarantees for Banks; Derivatives

When people buy a product or service, they generally care about the quality of the vendor from whom they are buying. They want to buy from someone who stands behind their products and offers some level of quality guarantee, and who will remain in business to back that guarantee.

However, there is, again, a single business for which this is not the case: banks. Most people bank where it is most convenient for them based on the location of bank branches. Few take any interest in whether the bank is operating in a sound financial manner because they believe their deposits are covered by a government guarantee. So if the bank goes bankrupt, government deposit insurance will give them their money back.

The banks claim this is fair because, in many countries, they pay money into an insurance fund that backs people’s deposits. But these insurance funds typically have less than 1% of the deposits they are insuring. When there is a crisis of confidence in banks, that less-than-1% isn’t remotely enough to cover deposits of failing banks. But as shown during the phase of the financial crisis in 2008-2009, governments go far beyond these bank deposit insurance funds to protect banks, calling them too big to fail, and thus, money is borrowed or printed to keep the banks afloat.

This unique arrangement for banks allows them to engage in highly risky financial maneuvers that are unavailable to others. The most egregious area for this type of behavior is in what are called derivatives. These complex contracts provide insurance against—and allow people to gamble on for potential profit–nearly every conceivable movement of interest rates, currencies, stocks, commodities, and so forth. But because of this unique government backing, banks are allowed to sell this wide-ranging insurance with nowhere near the reserves that would be required were a regulated insurance company to sell the same coverage. Banks even sell insurance against governments going bankrupt, including their own, even though their ability to make good on such contracts could only possibly come from the government whose debts they pretend to be insuring. To give just a hint of the size of the risk involved with these derivatives, the largest US and European banks have risk exposure to derivatives of hundreds of Trillions of US Dollars, almost ten times the size of the entire world economy.

Selling these derivatives is extremely profitable for the banks, so these absurd levels of risk are tolerated and excused away. Many derivatives are, in fact, a blatant form of fraud since seller could not possibly make good on these contracts. But since it is bankers who in fact write the laws for these contracts, it is all “legal.” While things are going well for the banks selling these contracts, they pull in staggering profits from this activity. When these bets go wrong, the burden of the losses is placed on the taxpayer.

To give an idea of this in numbers, as an example, at the end of 2014 in the US, the bank deposit insurance fund held $52 Billion, insuring $6,200 Billion in deposits (119 times the insurance fund), and backing $239,000 Billion In derivatives (4,596 times the insurance fund).

In addition, it is the trade in derivatives that now move prices in global markets for many commodities, including essentials such as oil, wheat, and corn. The value of trade in derivatives for a commodity can be 100 times larger than the value of trade in the actual commodity. Thus prices are often set through derivatives, not through trade of the actual physical commodity, allowing prices to be moved far from the fundamental value of the commodity, and offering opportunities for outsized profits from magnified price movements that can have severe negative effects on the producers and consumers of essential goods.

Furthermore, many derivative trades are private transactions between parties, often defined by complex contracts that are hundreds or even thousands of pages in length. Efforts to bring all of these trades into the clear light of day on public trading exchanges have been successfully resisted by the large banks, offering the potential for illegal manipulation of markets, yet another potential source of outsized profits.

Financial Domination of Politics

Increasingly, because of the need for massive campaign funds in modern electoral politics, the political class is beholden to those who provide what are politely called “donations” or “contributions” to campaign coffers, but which have become difficult to distinguish from bribes.

Increasingly, national and major state/provincial electoral politics looks like this: prospective candidates meet with extremely rich potential contributors to secure startup campaign funds and the funding promises needed to mount a full campaign. It is at this step that candidates are actually selected—often by billionaires. After this step, actual campaigns are carried forward, first among entrenched party operatives, and finally the campaign is brought to the public where many if not most people often feel like their vote–if they bother to cast it at all–is being cast for the “lesser of two evils” or for “the devil we know versus the devil we don’t.”

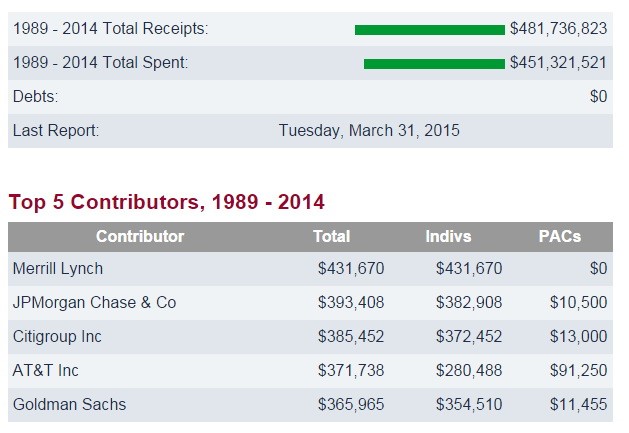

As an example, here is the fundraising and spending from 1989 to 2014 of a single US Senator, John McCain:

(Source: OpenSecrets.org)

So, over the last 25 years, Senator McCain raised and spent almost a half billion US Dollars on his campaigns. And four of his five largest donors are from Wall Street. What are the odds, when any matter relevant to banking or markets arises, that McCain would listen to concerns of you or me, or even a large group of us, versus the concerns of Merrill Lynch, JP Morgan, Citigroup, and Goldman Sachs?

This close connection with contributors increasingly extinguishes differences, once in office, of the actions of the various political parties, regardless of pre-election campaign rhetoric. In other words, once in office, this political class, regardless of party affiliation, enhances the positions of those already in charge of the status quo in almost every respect because all too often, it is doing the bidding of its donors, who often provide major funding to all prominent political parties. If a prominent member of a political party challenges a funding industry, that industry will threaten the entire party with denial of funds:

Four “Too Big to Fail/Jail” Banks Threaten to Hold Back Funds to Democrats Over Elizabeth Warren

Thus, substantial portions of the huge flow of tax money discussed above are not used to serve the people but to increase the profits of those sectors of the economy that already have sufficient funds to be among the largest of campaign donors, seriously widening wealth inequality in the society and, in effect, taking from those who have less for the benefit of those who already have much more, enabling the very rich to purchase even more political influence and to further entrench the existing political elite. Some label this “crony capitalism,” but it is not capitalism at all, it is theft and oppression by a small, oligarchic class that has learned how to manipulate the system for the personal gain of a small group.

The Revolving Door: This stranglehold on government by big-money interests is further cemented by what is called the revolving door policy. This is the movement of personnel between roles as legislators and regulators and the industries supposedly subject to the legislation and regulation. The excuse for this policy is that industries are now too complex to be regulated by those who are not industry insiders. This enables members of an industry to write, approve as law, and enforce the legislation and regulations that are supposed to assure the fair play of those industries within the society but which instead guarantee substantive advantages and large financial flows to these industries.

Conclusion

Is this picture becoming clear? We have structures in the world where:

- Banks (commercial and central) can create money with zero effort while the rest must work for it, often with great effort;

- People are laboring under a tremendous burden of income, sales, property, and utility taxes and fees that can take 50% or more of their income; much of this tax money flows to those who have the means to strongly influence, if not outright control, government actions to assure that even more of that tax money flows in their direction;

- Debt has become so integral in government, business, and personal financing, and in the creation of all products and infrastructure, that 30% of the price of almost all products is due to interest expenses in the supply chain; if people take on personal debt in the form of mortgages, car and student loans, or credit card debt, then their personal interest expense burden is even higher; this leads to a massive flow in interest payments paid by everyone but concentrating in the hands of a small group who use that money to buy up large portions of the productive resources of the planet;

- Any money saved constantly loses purchasing power by design, pressuring people to spend, borrow, and to put their savings into risky assets;

- When all money is loaned into existence, it forces organizations into a growth-at-any-cost mentality that threatens crucial natural systems that support our life;

- People are born owing a substantial sum of money that is part of an ever-growing national debt that can never be fully repaid.

- Ideas to undo structural unfairness are rarely even part of the political debate, and if they do surface in public, are quickly squashed by the entrenched political and financial elites.

Is it any wonder that the vast majority of people on this planet are struggling financially? They are placed under a tremendous burden of debt and taxation from the moment they are born, and any money they save inexorably loses purchasing power.

The overall effect on people is twofold:

First, if an economy based in fairness can rightly be called the voluntary exchange of service for service among people, what people see is that some players in the economy receive a service without rendering one in return. They see that some of these players become vastly rich in the process and that they then strongly influence the political process to tilt the entire economic table even further in their direction. With such examples on full display, more and more people focus their efforts on getting something for nothing, on gaming the system rather than producing real value that they can rightfully exchange with others in the marketplace. People with money increasingly focus on making money from their money in the world’s giant financial casinos through stocks, bonds, currencies, commodities, futures, options, cryptocurrencies, and so forth. They don’t see debt as a burden that depresses future expenditures, they see it as a way to get rich from other people’s money, and seek to qualify for as much debt as possible. A home is no longer primarily a place in which to live, it is now an asset class to be re-modeled for resale value, flipped, and borrowed against to meet expenses or to make even more money in other asset classes. People along the entire financial spectrum seek handouts from government programs and jump through hoops, sometimes less-than-legal hoops, to avoid taxes. People see the richest using tax loopholes to pay a smaller percentage of their income in taxes than a typical worker. People see that those with money can bully the courts and regulatory systems into allowing them to get away with illegal actions—perhaps, for truly egregious actions, they receive a fine that is small compared with the profits earned from outright illegal activity–and thus clever lying becomes honored in the society.

In a society where the money is created from nothing by a small group, getting money for nothing, generally through tricks and sometimes by lying, becomes the focus of more and more people. The economy becomes an increasingly hollow competitive shell of money chasing money wherein there are always “winners and losers” rather than a vibrant, productive joint effort based on a cooperative win/win approach for all.

Second, when all money is loaned into existence and thus all money is debt, and interest must always be paid on that money, there is always a general feeling of not having enough, or a fear of perhaps not having enough right around the corner. Everyone falls in with the environment-endangering growth-at-any-cost mentality since standing still economically does not feel like a valid option to people when interest must always be paid, the paper/electronic currency constantly loses purchasing power, and taxes must be paid at every turn. This gives rise to a feeling of scarcity in a world awash in abundance and leads to the feeling that people must compete with others for scarce resources or they will die starving and penniless in the street.

IT DOES NOT HAVE TO BE THIS WAY! This is a set of structures intentionally designed by a small group of insatiably greedy conscienceless people using us and nature as cannon fodder and who have commandeered academia and the mass media to convince us that it must be this way, that in fact this way is glorious. It is not. Structural unfairness is not inevitable. We have the know-how, power, ability, and to make this world a far, far better place.

* * *

Thank you for reading this series of posts on the structural unfairness of our current system. I look forward to your comments.