Most people likely heard that on December 15, the US Federal Reserve raised interest rates for the first time in nine years. Nine years! And by a measly 1/4 of a percent. With high Madison Avenue puffery, they called this “liftoff”! And why now? Because, they claim, finally, after telling us at the end of every year, for the last six years, that the economy would accelerate in the new year and be able to grow on its own without their “extraordinary measures” (their phrase, not mine) of support, they are declaring, like Bullwinkle, “This time for sure!”

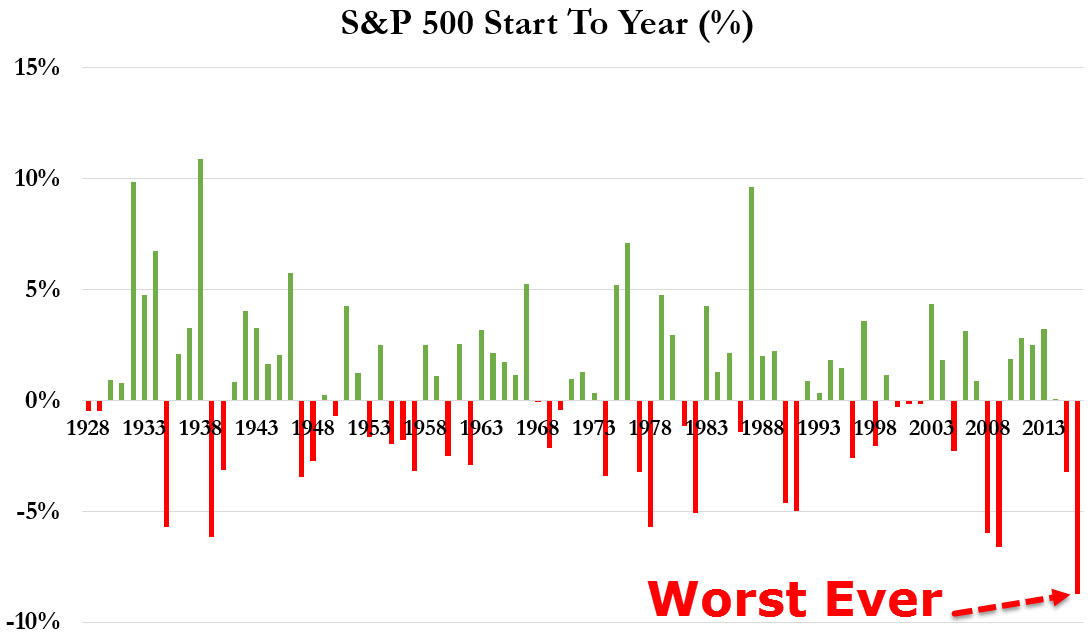

Stock markets are, of course, throwing a tantrum, off to their worst start to a new year ever, screaming, “What?! No more free money for the rich?! You mean we’ll actually have to do something to get money, like–uuuugh–poor people do?”

(Chart source.)

Worst start ever for other countries as well, including Europe as a whole. The 600 largest European stocks (EuroStoxx 600) are down 21% from their peak in April, officially qualifying them for a bear market. Same with China, their stocks lost 21% in the last four weeks (since the Fed raised rates) and are down 44% since their peak in June:

China Stocks Enter Bear Market, Erasing Gains From State Rescue

Stocks in emerging market countries (Brazil, Thailand, South Korea, Malaysia, etc.) peaked in Autumn 2014 (!) and are down 36% since then. This was posted in August:

23 Nations Around The World Where Stock Market Crashes Are Already Happening

Still, many people, especially in the US, believe we are in a global bull market in stocks; despite the fact that US smaller company stocks (Russell 2000 index) are down 22% since their peak in June, 2015. And US Transportation stocks (truckers, airlines, shippers, etc.), which are an excellent barometer of economic activity, are down 28% since their peak.

Even in the midst of this stock market tantrum, a desperate US President said last week that everything is awesome and that “Anyone claiming that America’s economy is in decline is peddling fiction.” Forget about those 45 million US residents on food stamps, and a record number of homeless children, everything is supposedly great. And there was this desperation from the Fed on Friday:

January 15 – Bloomberg (Matthew Boesler): “The U.S. economy should continue to grow faster than its potential this year, supporting further interest-rate increases by the Federal Reserve,” New York Fed President William C. Dudley said. ‘In terms of the economic outlook, the situation does not appear to have changed much since the Fed’s Dec. 15-16 meeting,’ Dudley said, in remarks prepared for a speech Friday… He added that he continues ‘to expect that the economy will expand at a pace slightly above its long-term trend in 2016…’

(Digression: Only someone involved in pseudo-scientific economics is typically deranged enough to try to explain how something can “grow faster than its potential.” Perhaps we should each send our favorite economist a dictionary.)

Why do I call these statements desperation?

For starters, the Federal Reserve’s best computer model for the economy says that the economy is growing at a 0.6% annual rate. That’s less than 1% a year, folks. In other words, stall speed.

JP Morgan says it’s less than that. They expect 0.1%:

Recession At The Gate: JPM Cuts Q4 GDP From 1.0% To 0.1%

I’ve talked here before about the usefulness of economic statistics that governments don’t publish since the governments can’t fake them. I won’t bore you with a lot of them, but here’s one that will give you an excellent idea of the state of things. It shows, over the last 30 years, the cost to companies to transport bulks goods (wheat, copper, coal, oil, iron ore, etc.) by cargo ship around the planet:

(Chart source.)

The first thing to notice is that it costs less to ship cargo now than it has at any time in the last 30 years. And it’s cheaper by a wide margin. If the economy were doing well, cargo ships would be in high demand and charging high prices. That’s hardly the case now; quite the opposite.

Next, check that blue oval at the top of the chart. The index was over 10,000 in early 2008. That was a period of high demand for shipping. It’s useful to know that owners of large ocean-going cargo vessels currently break even when the price they can charge for shipping is between 800 and 1,000 on this index. So with shipping costs as high as they were in 2008, the owners of ships were making a LOT of money–they could charge more than 10 times their expenses for fuel, salaries, maintenance, etc. Now the price is below 400. So the ship owners lose money on every shipment. Competing owners of cargo ships continue to ship at these low prices, even though they are losing money, because they hope their competitors will go bankrupt before they do.

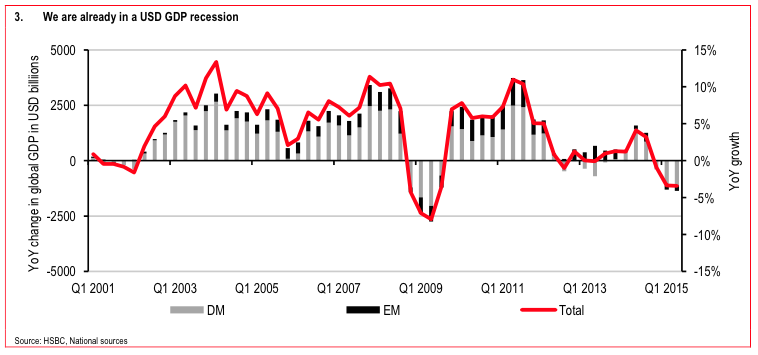

Why is it so cheap to ship goods around the world now? Because global trade and the global economy are tanking, and far fewer goods are being shipped than a few years back. Here’s a chart by HSBC of growth of the global economy calculated in US Dollars. Notice that the line is well below zero for 2015, just like it was in 2009:

Credit Suisse expects Brazil’s economy to have its worst downturn since 1901! That’s right, worse than the Great Depression. As shown by the chart at the link, India’s exports and imports both crashed by 25% over the last year. That’s a huge decline.

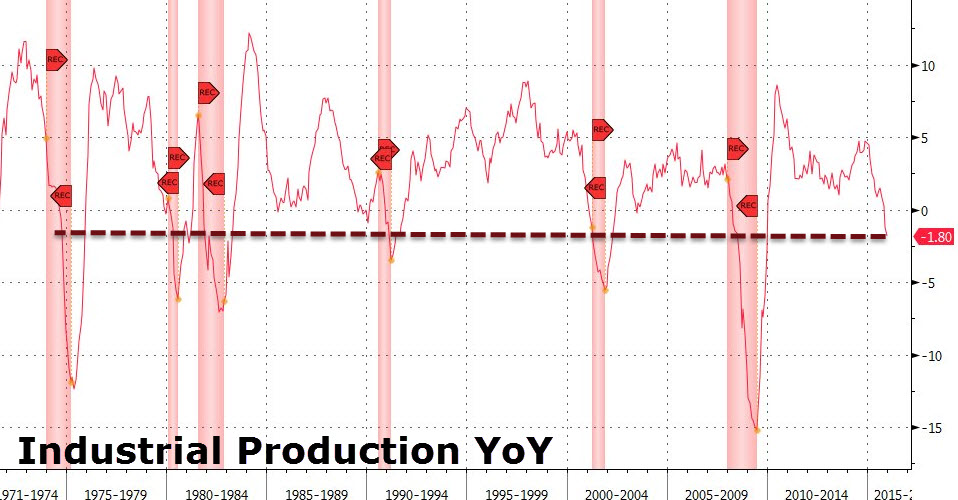

So the Fed and other cheerleaders might say: Yes, the world economy is down, but the US has “decoupled” from the world and is doing fine on its own. Well, here’s a perfect depiction of the US economy. It’s a chart of US Industrial Production over the last 45 years:

(Chart: Welcome To The Recession: Industrial Production Crashes Most In 8 Years)

Industrial Production in the US is down over the last year; there’s 1.8% less of it than a year ago. The red-shaded areas on the chart are past recessions. As the dashed line shows, whenever Industrial Production has been this low in the past, we have always already been in a recession. Always. No exceptions.

Governments (and 99 out of 100 economists) announce recessions with a huge lag time. Leading up to the announcement, just when it would help people to be battening down the hatches, they always claim everything is fine and there won’t be a recession, so we should all hold onto our stocks, hold onto our real estate, spend, borrow, and spend some more. Then the long delay in admitting to the recession allows them to say, “Yes, a recession started 10 months ago, but now it’s either over or almost over, so don’t worry, everything is fine. Spend, borrow, and spend some more.”

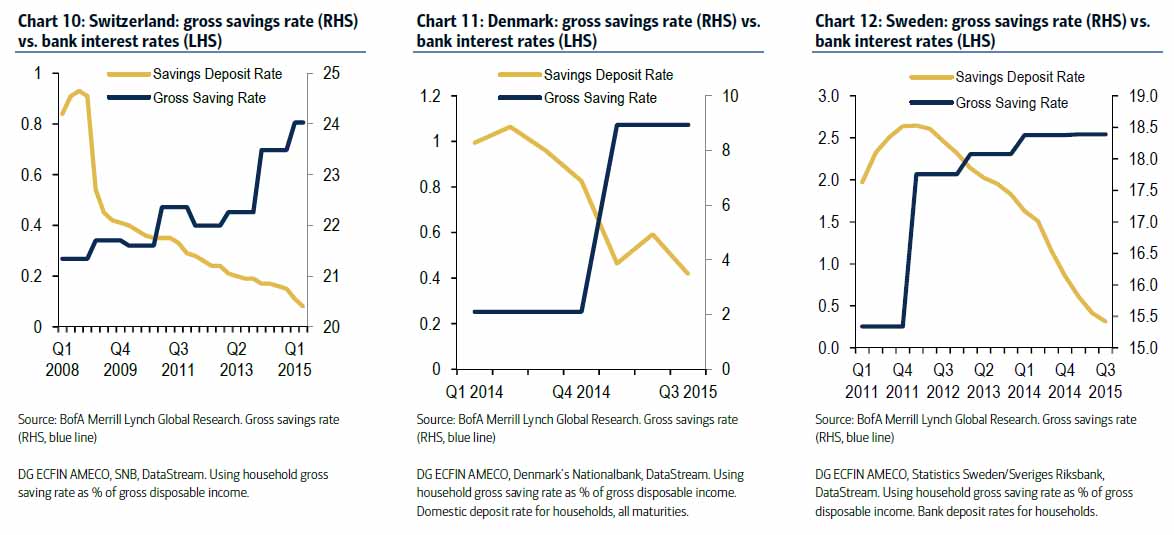

The Fed’s Dudley also said this week that, if the economy weakened, they would consider negative interest rates for the US. Canadian central bankers say the same. And it has worked so well in Europe! (Ha!) Europe’s delusional central bankers thought that negative interest rates would spur people and companies to save less and spend more. What actually happened? Bank of America explained here that as rates went negative and people couldn’t earn interest on their savings, they saved more, not less. In other words, people, unlike the delusional bankers, are being logical: if they can’t earn any interest, then they have to save more for their future plans, not less. Here are the charts showing exactly this relationship (as rates go down, savings go up) for the negative rate champions Switzerland, Denmark, and Sweden:

European business also failed to fall for the negative rates trick. Instead of borrowing and spending more, they have been pulling in their horns and retiring some of their outstanding debt instead of borrowing more.

As Michael Burry of The Big Short said in his speech at UCLA:

The individual can think different and the individual can act different than those that got us all into this mess. No matter how the economic tides may sweep away the majority, an individual can stand clear.

More than ever, it is crucial to understand that “society’s sanctioned suits,” as Burry labels them so well, do not have your best interests in mind. They have their own interests in mind. Period. And their desperation, delusions, and derangements have created an inevitable economic calamity that will be the greatest in history.

Burry is right: Stand clear!