At base, the world has a true financial system consisting of people producing goods and services with real value and trading those among themselves. But grafted onto that reality is an intentionally complex and confusing mega-structure built from a series of promises that are lies. As these promises are increasingly understood as lies, this mega-structure is proceeding inevitably down a path to disintegration. The primary purposes of this article are:

1. To provide you with a checklist so you can understand where we are in this process of financial system disintegration. There is a caveat in terms of using this as a serial checklist proceeding over time: more than one of these lies may get generally recognized in a single event, with understanding rapidly communicated to the entire world.

2. To forearm those who wish to prepare with an understanding of what is unfolding. This is a predictable process, but it may feel quite chaotic to the unprepared. With understanding, and with echoes from the words of the immortal Rudyard Kipling, you will be able to keep your head (and your heart!) when all about you may be losing theirs.

3. To encourage people to take simple steps to sidestep the consequences of the widespread recognition of these lies. It is important to understand that general recognition of just one of these foundational lies–the lie that real estate prices always go up–came within hours, in October 2008, of vaporizing almost all of what are considered to be assets in this financial regime. Evasive action needs to be taken before these lies are generally understood. It is better to do your run on the bank before everyone else decides that’s a good idea. Those who prepare will be able to provide some assistance to those who have not.

4. To allow readers to proceed from understanding, not from the fear that leads to panic, and not from the fear that leads to denial or to throwing up one’s hands and pretending there is nothing to be done about all this. We hope this article provides such understanding.

In terms of tracking this process, we have already seen one prominent lie from this system bite the dust:

Lie #1: Real estate always goes up.

The perpetrators of this lie trotted out pithy sayings about population always increasing and “they aren’t making any more land” to somehow prove that real estate prices always go up. People can’t be blamed for this erroneous belief. Many saw real estate prices rising for their entire lifetime. But if one takes a larger historical look, it is obvious that real estate prices obey the Law of Cycles. They rise and fall just like most prices. This cyclical behavior of prices would not have been a problem for most people except so many of them fell for the idea that they should buy one or more properties with borrowed money, with a mortgage. So when prices fell, the amount owed on the mortgage has turned out to be greater than the current value of the house. Which is a nasty problem because, if a person wants to sell such a house, the current sale price is less than what they owe, so they have to pay money to sell their house, money which many don’t have. So they lose their house in a short sale or foreclosure.

For those who now have the urge to bet that real estate prices have fallen enough, the evidence says it’s a bad bet if you are thinking you will get price appreciation. If you are buying with cash to navigate through tough times, that is, you are buying a place where you can grow your own food, produce your own electricity, pump your own pure water, cut wood to heat your house? Good idea, depending, of course, on price and location. But buying or holding real estate thinking that the price will rise? Bad idea. There’s lots of evidence that any miniature “bottom” in prices will be short-lived and that prices will fall for a generation. The main reason? Real estate prices are still floating on a sea of debt. Most governments are still propping up otherwise-dead mortgage markets with government loans and guarantees that only a fool, excuse me, a government, would make. In other words, these are uneconomic loans that no sane person would make, and these insane loans are still propping up real estate prices in a big way. It won’t last.

************

The remaining lies are in various states of disarray, but all still play key roles in the mindset that keeps the system intact.

Lie #2: It’s best to use Other People’s Money.

The farther in time we progressed following the 1930’s—the last time there were worldwide losses of homes, farms, and business to foreclosure, the last time governments defaulted on their bonds en masse, the last time there were huge numbers of bank failures—the more people were convinced that saving up money in order to buy something was for morons, and that buying things now, on credit, was the smart thing to do. The big deal became just how much borrowing one could “qualify for.” (This disease still persists for some, which is why, despite all of the pain it has inflicted, Lie #2 has not been relegated to the past in this article.) Paying it back was simple: money was worth less and less over time, everyone knew that; salaries always rose; the price of houses, the main collateral for loans, those always went up.

The result of this mindset is that so many people and organizations and even countries have become debt slaves to the bankers. To quote an anti-debt crusader in

Ireland: “Bankers want you to use your energy and your work to make their dreams come true.” Too bad more people didn’t know that before getting themselves so far into debt that it dominates their life.

Lie #3: We can buy cheap goods from countries that have cheap labor, and yet keep our much-higher salaries and benefits.

We’ve all heard for decades about how manufacturing, and in more recent years services, are moving from the developed world to the emerging markets. People in developed countries love to buy cheap goods from lands with ultra-low labor costs. But they expect their own salaries and benefits to remain the same or even increase. How can that be when the sources of income–that is, the jobs and profits and the tax base–that support that salary and benefits structure have moved to another part of the planet? This divergence between expected lifestyles and the labor required to support those lifestyles is bringing exponentially increasing strain to the developed countries. People and governments have tried to maintain their lifestyle illusions by borrowing more money than they can ever repay. They have used this borrowed money to try to bridge the gap between falling real income levels and their habitual spending. Much of the borrowed funds are coming from the countries currently doing all the work to produce those cheap goods. The signs that this attempt is coming apart at the seams are everywhere for those who choose to look.

Lie #4: Government pension and medical programs will deliver on their promises.

Many currently depend on government pension, medical insurance, and disability programs. Many more consider them an essential ingredient in their upcoming retirement plans. But as discussed in Lie #3, the tax base that supports these programs is rapidly eroding, and their funding assumptions were based on far shorter lifespans, lower medical costs, and flawed demographics in terms of the shrinking number of people paying into the system versus the growing number receiving benefits. And governments forcing interest rates to near zero in lame attempts to boost their economies means that pension fund assets earn far less in interest payments than expected. (This is a serious problem for private pension plans as well, most of whom still claim they can earn 8% on their assets a year on average, something very few are able to consistently accomplish. Without that level of earnings, they will not be able to meet their commitments.) If the liabilities of governments were calculated the way they are for businesses, the governments would be promptly declared bankrupt and hauled into court, where evidence of fraud would be a dominant topic.

Governments have four options regarding this slow motion train wreck:

- cut promised benefits;

- radically increase tax revenue;

- borrow even more money;

- print new money. (In the typical fashion of these times, they came up with a new name for this counterfeiting process of printing new money, they call it “quantitative easing.”)

Because the last two options on that list are the most politically palatable and the least painful to current voters, these are the options strongly preferred by politicians. They believe that telling the truth about this situation and taking responsible measures to put these programs on a sound footing would get them promptly kicked out of office, which is likely correct. So they take the borrowing and printing route because the pain from these is hidden from most people, and most of the pain is dumped on people’s children and grandchildren. Oddly, for all the noise people make about wanting to leave great things to their children, most people don’t care a whit about passing this huge government borrowing burden onto the children and grandchildren about whom they claim to care so much.

The problem with the borrowing and printing regime is that markets and people are increasingly catching on that: the borrowings are too large to be repaid; and the printing debases the money people have saved and earn, driving up the prices of necessities. Countries such as Greece, to whom the markets will no longer lend money and which cannot independently print money because of membership in the Eurozone, have already cut retiree pensions by two-thirds, and there are more cuts to come.

And while federal government programs have so far garnered most of the attention in terms of their unsustainability, most state, province, and city pension and insurance programs are no better off, and many are worse off, and they generally don’t have the option to print money. In the US, the Pew Research Center and others have estimated that state and local pension programs are underfunded by more than a trillion dollars. Yes, a trillion dollars is one of those numbers that is too large to comprehend. But the takeaway for anyone depending on these programs is that you will not receive the benefits you expect. And yes, when the bankers need a bailout or the governments want to fight yet another war, then it’s deficits be damned, they can easily come up with a trillion dollars. But when it comes to helping regular people, then it’s: “Sorry, we’d love to help you, but we can’t afford it, we have these deficits, you know, so we can’t help you.”

Lie #5: Your money is in the bank

The banking cartel loves to make you feel like they are rock solid and that the money you deposit with them is “in the bank,” safe and sound. As most actually do know, it isn’t. Or rather, only a small portion of it is actually “in the bank.” The rest, generally 90% to 95% of it or more, gets loaned out. (Or is used by the bank for speculative trading.) The bank pays you, at best, a paltry amount of interest on your deposit, and utilizes your money for something that pays them at a higher rate, and thus makes money from your money. And in many countries, governments assure us that banks are a truly rock solid place for your money by saying that, if the bank really messes things up and loses your money, the government guarantees that you will get it back.

This works quite well—until it doesn’t. This model of banking, the “fractional reserve” system, where only a fraction of the deposits are kept on hand, depends on the idea that not all depositors will want their cash at the same time, so most of the deposits can be loaned out. This is fine until a group of depositors needs that money, or they get frightened that perhaps the bank won’t have their deposit available for them when they want it, and they start a “run on the bank.” We’ve all seen pictures of what that looks like. Some of them show a well-behaved line of people waiting to get their funds. Other pictures show an angry, unruly mob clustered at the front door, perhaps bashing some bank windows. And if the bank has loaned out 95% or more of their deposits, it doesn’t take a large group of depositors to drain all the cash from the bank.

When this happens at a single bank, no problem. The government steps in with its guarantees and depositors are made whole up to the level of what the government guarantees. But in the Fall of 2008, we saw the start of a run on the banking system. Seeing the collapse of some banks and hearing rumors of many more, some people and corporations worried that the entire banking system was going kaput (it was!), and they started withdrawing all they could from the system. So governments quickly stepped in with far larger guarantee programs than had ever existed before, covering types of deposits, such as those in money market funds, that had never been guaranteed before. It was made clear that money would be printed to cover deposits, and so depositors calmed down and stopped their run on the system.

So the problem was solved, for the time being, by governments guaranteeing that the failure of private, commercial, corporate banks would not hurt their depositors. But now, those who astutely foresaw that the 2007-2009 phase of the crisis was coming, and warned about it loudly and clearly before it happened, see that people are rightly suspicious of government guarantees because it is becoming obvious that governments are broke. And who wants to rely on a guarantee from a bankrupt entity! More on this topic below at Lie #8.

The real problem for the banks is that they own what are called toxic assets. When the banks were perceived to be failing, it was because people knew that what the banks were counting as “capital” was losing value hand over fist and that, in fact, many banks, especially the big ones, actually had no capital left at all. Because of the political power of the big banks, governments attempted to solve this problem in three ways:

1) They let financial institutions lie about the value of their assets. They came up with accounting tricks that enable a bank to say that a loan portfolio is worth 100% of what they paid for it even if the collateral backing the loans, for example houses or shopping malls, is now worth far less than 100%. People call this the “extend and pretend” model. It is not a real solution, but it temporarily covers up the problem.

2) They buy toxic assets from the banks at full value and transfer the toxicity to the government. For example, the US Federal Reserve purchased $1.2 trillion worth of mortgage backed securities to take the losses away from the banks and to put taxpayers on the hook for the loss. People call this the “privatization of profits and the socialization of losses” model.

3) They lend them scads of short term cash to keep them afloat. Most banks in Spain would now be closed without the accounting lies from point 1 above and from hundreds of billions of euros worth of short term loans of newly-printed money from the ECB, the European Central Bank.

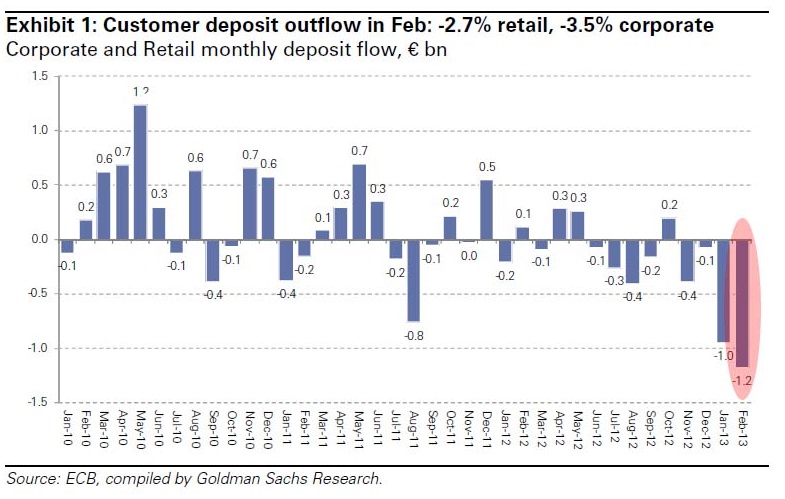

And in Greece and Spain, for example, some depositors are wising up. Billions of euros of deposits are being drained from Greek and Spanish banks each month, making bank solvency an even more distant hope with each passing month.

Lie #6: Your money is in your brokerage account.

Most people used to think–many still do–that brokerage accounts were safe from the fractional reserve threat to bank accounts, that is, they believed that brokerages did not lend out their money the way banks do, that their deposits to brokerage accounts just sat there waiting for deployment or withdrawal. Ha! Now that we are all wising up, how could we have thought that Wall Streeters could keep their grubby hands off that large pool of money. What the brokerages do is called the hypothecation of these assets, that is, they loan them out for a profit. And the entity, and I use that word intentionally, to whom they loan these assets often re-hypothecates them, that is, they loan those assets to yet another entity. It turns out that the City of London, an entity that operates quite independently of UK law in several respects, is the world playground of re-hypothecation, where the same asset can be re-lent several times. Have you wondered why it’s been so difficult for regulators to determine where the client money is in the recent failure of Jon Corzine’s MF Global brokerage? Look no further than the world of re-hypothecation, in which it can be difficult for anyone to know “where the money is” at any point in time.

So this is another part of the system where everything works well until it doesn’t. If people, intelligently I might add, start withdrawing significant amounts of money from the brokerage industry, they will find that it is yet another fractional reserve environment. So, is your money in your brokerage account really there? Maybe. Remember all that fine print they sent you when you opened your account that you didn’t read? Maybe that part about your account being a “Sweep Account”? Are the Wall Streeters sweeping your money for their profit?

Lie #7: It is OK for financial institutions to use huge leverage.

The Powers That Be/Were who run the financial regime think it is OK for central banks, commercial and investment banks, brokerages, and hedge funds to operate using massive leverage, in other words, massive borrowed funding. The system allows the likes of the Goldman Sachs, Bank of America, and Deutsche Bank to borrow tremendous amounts of money. In normal times, these big banks are considered reliable borrowers; when times are difficult, they are presumed to be backstopped by their governments.

The huge banks routinely operate at 20 to1 to 50 to 1 leverage. 50:1 leverage means that, for every $2 of reliable capital they have, they can operate in the marketplace as if they have $100. So a 2.5% loss wipes them out, makes them insolvent. In world markets operating at ever-increasing speeds, how can any participant always avoid a 2% loss? They can’t. Thus the financial system goes from crisis to crisis. As long as such large-scale leverage persists, the next bubble, and therefore the next crisis, will never be far off. Big leverage was at the base of every major crisis of the modern financial era: the Crash of 1987, the LTCM debacle of 1998, the tech stock crash of 2000, and the real estate bubble.

So why is this allowed to persist? Because these influential institutions can make a lot of money using leverage when times are good. Money they can use to influence the political and regulatory process. And when times are bad? Their losses are taken over by the taxpayers. Heads they win; tails we lose.

And consider what happened, and continues to happen, in the real estate market, when a buyer only has to come up with a 2% down payment. That means they are operating at a leverage ratio of 50:1. This has worked out very poorly for buyers and lenders. Yet in the USA, the government agency known as the FHA still guarantees hundreds of billions of dollars worth of real estate loans each year where the buyer only needs to come up with 3.5% as a down payment.

Lie #8: The government guarantees it.

Governments love to guarantee things. It makes people feel good, thus helping to secure votes, and typically it costs nothing up front. It’s a politician’s dream. So governments guarantee all kinds of things: bank deposits, mortgages, private pensions, student loans, loans to build what no sane person would build such as nuclear power plants, the bonds for infrastructure projects, loans made by a zillion government agencies, zombie banks (ones that would be promptly out of business if they weren’t being propped up by the government), companies considered too important to be allowed to fail, export-import loans, mortgage-backed securities…the list is long. And we have seen it expand promptly when an emergency hits.

But now people are questioning these guarantees. Iceland actually allowed citizens to vote on some of their government guarantees when the payments actually came due…and the people promptly threw those guarantees out. Guarantees in Ireland are on very thin ice. Very few trust government guarantees in Greece. Portugal, Spain, and Italy are likely next on the docket. In the past, very few people calculated these guarantees as part of government debt because they assumed that a guarantee was sufficient, that because of the guarantee, no money would ever have to actually be paid out. Now some of these guarantees are taking a big bite from government budgets. In the US, billions are being paid quarterly from government coffers into mortgage monsters Fannie Mae and Freddie Mac to cover losses on guaranteed mortgages.

Note that the public questioning of guarantees is mostly now happening in Europe because the individual countries in question do not have the authority to print new Euros. But the fact is that finances in Japan, the US, and the UK are worse than those in some European countries, but because these countries can print money at will, which they are also doing in volume, people still “trust” their guarantees. It is worth considering whether such trust is well-placed when printing trillions is required to keep the guarantees intact. People and markets will ultimately decide that it is not. It is best to stay ahead of this curve and to understand whether your bank, your pension fund, or any institution on which you rely is on a sustainable path. If it is not, make other plans as well as you can. And take action soon.

Let’s take a break! In tomorrow’s Part 2, we will cover these lies:

Lie #9: Government bonds are safe.

Lie #10: Derivatives reduce risk in the system

Lie #11: Central banks protect the interests of their country and its citizens

Lie #12: Your paper/electronic currency is a reliable store of value.

Many thanks.

Thundering Heard