(Note: As explained here, this is a draft of a chapter in an upcoming book on vanquishing financial problems once and for all.)

AVOIDING STRUCTURAL UNFAIRNESS

In a condition of societal financial collapse, and its associated privations, people are understandably desperate to reinstate that which prevailed before the collapse. This is a poor choice when that which is familiar is inherently flawed in ways that:

- made financial collapse inevitable and,

- caused a great deal of unnecessary pain prior to the collapse due to structural unfairness in the financial system.

Thus, to avoid creating a future that necessarily includes the pains resulting from structural unfairness (among people, businesses, and regions) and inevitable financial collapse, it is crucial that we all understand the preventable flaws of the modern financial system to assure that these flaws are not reinstated. Repeating these flaws guarantees a world where a very few have great wealth, where a very large number of people struggle daily for basic necessities, and where the vast majority works daily to provide more for the very wealthy few.

The Problem: Structural Unfairness, an Executive Summary

It is essential that people understand this concept of structural unfairness. Allowing structural unfairness means there is no “level playing field” for all parties. It guarantees ever-growing and societally destructive wealth inequality. This is not wealth inequality based on inevitable differences in financial effort and talent among people, this is severe inequality that is built into the system. That is what is meant by structural.

Here are some conclusions to this section, to be followed by the supporting details:

- Most people and industries work diligently to produce a product or service from which they earn money. Yet one industry, banking, can create money from nothing, lend that money to others, and charge interest on that new money. It is virtually guaranteed that this single industry with access to free money will come to dominate the economic and political worlds.

- Many people in the world work hard to obtain what is considered a good salary, a steady income. But when they achieve that goal in developed economies, between national, state/provincial, county, and municipal taxes on their income; VAT, sales, and fuel taxes on their purchases; property taxes; and agency taxes and fees (for example, on telecommunications and utility bills); for many, at least 50% of their income is taken.

- In an economy in which most businesses in the vast supply chain that provides the world’s products and services have taken on debt in their businesses, according to those who have studied it, on average, 30% of the cost of everything people buy is due to interest expenses in the supply chain.

- Because governments borrow money to fund infrastructure projects, the cost of building roads, bridges, schools, airports, stadiums, and so forth would be, on average, 40% less were it not for interest expenses on the debt for the project.

- If a person in this economy takes on one or more forms of personal debt–mortgage, car loan, student loan, credit card debt, and so forth—yet another substantial chunk of their income is consumed by interest payments.

- Because almost all governments have made promises they cannot keep and which are not sufficiently funded by taxes, they borrow ever-increasing amounts of money. From 1988 through 2014, the US federal government, for example, paid US$9.4 Trillion in interest on its borrowings, so a substantial portion of the US$18 Trillion national debt (in early 2015) is due to accumulated interest payments. Furthermore, these vast and accumulating government debts mean that all children are now born with a portion of the nation’s debt burden they are expected to pay so that the lenders can continue collecting interest payments; in the US as of early 2015, each child is born with a national debt burden of more than US$57,000.

- Who collects these vast flows of interest payments? Those who can create money from nothing, that is, the banks; and those who have excess assets to lend. According to those who have studied it, 60% of the massive flow of global interest payments go to the wealthiest 10% of the populace. And we all now know from more detailed studies that these massive money flows concentrate further within that 10%, especially to the 0.01%, who then use those money flows to have a major influence on government and media, thus controlling the laws under which people live and the messages with which they are constantly bombarded by television, radio, and in print.

- High taxation and heavy government borrowing go hand-in-hand with massive expenditures by government. Those businesses that continuously benefit from these expenditures use profits to influence elections, elected officials, appointments at regulatory agencies, the writing of laws, and media coverage of issues, continually increasing the flow of government expenditures in their direction at the expense of taxpayers and the rest of the business community. Thus, the banking cartel, the military-industrial complex, the medical-industrial complex, and so forth, become permanent, major fixtures in government budgets, strong voices always moving policy in a direction favorable to their business prospects.

- The fact that all money is now loaned into existence by either a commercial or central bank means that all money is debt that carries an interest payment that must be made. This means the economy must always grow so that the loans plus interest can be paid. When the economy stays stable or shrinks, some are unable to pay their loans plus interest and money starts to disappear from the ledgers of the lenders, leading to the banker-dreaded “deflation.” Because of this debt-based money, our economies are inherently unstable and thus we hear the endless chants for “growth, growth, growth.” But what is the impact of this quest for infinite growth when our economies are powered by finite resources such as fossil fuels, iron ore, cement, fertilizers for industrial agriculture, and so forth? As we watch our growth-at-any-cost approach accelerate the extinction of species around us—many of whom provide crucial support for humanity—how long will it be before we threaten our own species?

- If a person tries to save money to gain independence from this structural treadmill, their savings constantly lose purchasing power by design, pressuring them to spend, borrow (which they can pay back later with cheapened money), and to put their savings into riskier assets “to keep up with inflation.”

- If a person or group attempts to operate financially outside of this web of debt, they are punished by legal tender laws that, while appearing innocuous, go a long way toward locking them into the system. The legal tender laws say that any debt can be satisfied by payment in the legal tender currency. If a person tries to operate using gold or silver or bitcoins, these forms of money are considered by the system not as legal tender, but as assets. Thus, when they are sold–for example, if you buy a cup of coffee using a fraction of a bitcoin or a barter currency—this is the sale of an asset and thus some governments want to know whether that bitcoin gained in price from the time you purchased the bitcoin to the time you “sold” it to buy coffee. And they want to tax you on any gain. Thus, alternatives to the government fiat currency such as gold and silver go into hiding in vaults as forms of savings and are not used for transactions.

- Attempts to undo structural unfairness rarely surface as part of the political debate, and if they do, it is the voices of those providing the bulk of financing for expensive modern political campaigns that are heard and heeded, increasing structural unfairness rather than undoing it.

While this is not the complete picture of the structural unfairness in our current system, let’s take a quick look at the finances of someone who is “doing well” according to the world, that is, earning what is considered to be a very good salary. Between national, state/provincial, local, property, VAT, sales, fuel, and agency taxes and fees, at least 50% of their income is directly taken. Then, of almost everything they buy, 30% goes to interest expenses. If this person has any debt of their own—such as a mortgage, automobile or student loan, or credit card debt—then another serious portion of their income is dedicated to interest expense. Any money they save constantly loses purchasing power. Is this person really “doing well”? Or have they been enslaved by those collecting taxes and interest? If the minority on this planet that are said to be “doing well” are often in or near financial difficulty, what about the vast majority, the billions of people who do not have that “very good” salary?

Is this beginning to sound like a movie about a criminal syndicate that collects “a piece of the action” from all businesses in an area? For the “protection” of those businesses? It should: the analogy is not far-fetched. The structures described above—structures through which a portion, a “cut” is taken of nearly every transaction in the economy—are not accidental, they are intentional:

When plunder becomes a way of life for a group of men living together in society, they create for themselves in the course of time a legal system that authorizes it and a moral code that glorifies it.

—Frederic Bastiat, The Law, 1848

Structural Unfairness, the Details

In early 2015, OXFAM showed that by the end of 2015, “1% of the world’s population will own more wealth than the other 99%.” In other words, the richest 1% own half of the world’s wealth. In early 2015, just 80 people owned the same amount of wealth as the poorest 3.5 billion people on the planet. And the trend toward extreme wealth inequality is accelerating, with the wealth of those 80 people doubling between 2009 and 2014.

This is not accidental, this is by design.

The major structural problems that relentlessly add to this extreme disparity will be shown in these sections:

- Money Creation by Banks

- Taxation

- Money that is Loaned into Existence

- Money Designed to Lose Purchasing Power

- Government Borrowing

- Governments Borrowing Money into Existence

- Growth at any Cost

- Legal Tender Laws

- Government Guarantees for Banks; Derivatives

- Financial Domination of Politics

Money Creation by Banks

One primary source of structural unfairness is granting bankers—both commercial and central bankers—the license to create money from nothing and to charge people for the use of that money. A bank does not lend cash from its vaults, it creates ledger entries that create money.

The process by which banks create money is so simple the mind is repelled.

–John Kenneth Galbraith, economist, professor—Harvard University

Commercial Banks

Let’s say you sign up for a four-year car loan from a Bank A. Bank A now claims it has an asset—your promise to repay the loan. It creates a ledger entry recording the fact that you will be repaying the loan with interest in installments over four years. So for the next four years, each month, you pay the bank a portion of the money you borrowed plus some additional money as interest, the fee the bank charges you for renting money from them. (If you don’t pay, the bank will claim your car by repossessing it.) If the car dealer is also a customer of Bank A, then the car dealer’s account is credited with the amount of the loan. That’s it. The transaction is done. The money has been created and you are charged interest over the life of the loan for the use of that money.

If the car dealer’s account is at Bank B, an electronic transaction is created that credits the car dealer’s account at Bank B. Of course, like Bank A, Bank B has been busy creating car loans, mortgages, and business loans that day. At the end of the day, all of the electronic credits between Bank A and Bank B are totaled up (by a clearing organization—for example, the Federal Reserve in the US) and whichever bank is owed money receives a credit for that money and the paying bank has a debit. In reality, even though both banks possibly created a lot of money that day, the balance between the banks, the difference at the end of the day, is relatively very small in practice.

Here is a quote from Robert B. Anderson, Treasury Secretary under US President Eisenhower, in 1959:

When a bank makes a loan, it simply adds to the borrower’s deposit account in the bank by the amount of the loan. The money is not taken from anyone else’s deposits; it was not previously paid in to the bank by anyone. It’s new money, created by the bank for the use of the borrower.

And here is one from the Bank of England in its quarterly bulletin in the Spring of 2014:

The reality of how money is created today differs from the description found in some economics textbooks: Rather than banks receiving deposits when households save and then lending them out, bank lending creates deposits. . . Whenever a bank makes a loan, it simultaneously creates a matching deposit in the borrower’s bank account, thereby creating new money.

Yet both Bank A and Bank B can charge interest—the continuing rent for borrowed money—on all of the money they created that day. Alternatively, the bank might package up most or all of the car loans they made that month and sell that package to another party, perhaps a pension fund, who pays the bank a hefty amount of cash for the right to receive the interest payments on all of those car loans over the next four years. In this case, the bank receives a hefty cash payment for all of the money it created from nothing for car loans during that month.

So for doing some fairly straightforward computer processing, the bank received quite a lot of money. It might have also packaged up and sold the business loans and mortgages it created as well. Or it might keep any or all of these loans and collect the interest each month. Either way, since so many believe that they need that money loaned to them by the bank, the bank makes a huge profit from something it created from thin air because it has the license to do so.

Clearly, it is vastly easier for a bank to accumulate money than it is for people and other businesses to do so. All others typically need to work hard to provide useful products or services to earn money. Is it any wonder that most city skylines are, if not dominated by banks, let’s just say that the banks are very well represented.

The credit card business is another highly profitable operation of banks for which they rarely need to use any of their own capital. It typically runs strictly off of the fees charged to vendors who accept credit cards. For those who want the details, they are explained in this article by Ellen Brown:

Usurious Returns on Phantom Money: The Credit Card Gravy Train

This ability of banks to accumulate money far more easily than others is a structural advantage that makes it inevitable that banks will eventually dominate both the commercial and political domains. Their access to free money makes it nearly inevitable that they will lend to favored businesses and governments; deny loans to those they do not favor; use outsized profits to participate in and dominate what are supposed to be free markets for stocks, bonds, currencies, and so forth; and use their profits to purchase political influence, thus writing laws that guarantee and enhance their privileged position, and placing those who favor the banking industry as government regulators.

Some argue that the public banking model—in which banks are a branch of the government and all banking profits fund projects for the public good—solves this structural advantage problem, even to the point of eliminating the need for taxation and government borrowing. We will analyze the Public Banking Model in a future post.

Central Banks

In almost all nations, the cash and base electronic money of the society is created by a central bank. (While cash may be printed at a mint, central banks currently control how much of that money makes its way into the economy.) This central bank, sometimes a private corporation and sometimes a branch of government, is granted the license, the concession, to create the nation’s money, most of which is electronic, and to manage the quantity of it in circulation.

In recent years, the central banks have engaged in what they call quantitative easing, but which is known in more honest circles as money printing. In this practice, the national government borrows money to pay those bills that it cannot cover through taxation by issuing various forms of government bonds, and the central bank creates electronic money from nothing to buy those bonds.

Prior to this, and in addition to it still, central banks created money in a variety of ways. For example, central banks of the West often create money through operations to add reserves to banks. Central banks in the East, in countries with large trade surpluses, create new national money to exchange for the foreign money that flows in from their exports. Foreign money is deposited into their commercial banks by their exporting corporations; these commercial banks want to exchange that foreign money for their local national money. The central bank then holds onto that foreign money as reserves. For example, we all hear about the central bank in China holding almost $4 Trillion in reserves.

In addition to the great power implied by being able to create the nation’s money from nothing, central banks have the power to manipulate interest rates, thereby strongly influencing the cost of borrowed money.

These powers have given them such influence over economies and markets that they are nearly considered gods in today’s world. Their public statements are awaited with bated breath and then endlessly analyzed and debated as if their words came “from on high.” Financial markets often have large, spasmodic moves because of a single word or sentence uttered by a central banker.

Furthermore, most central banks operate behind a veil of secrecy and often with no outside audit of their actions. They claim that this secrecy protects their independence from political influences. However, this secrecy enables massive abuse of this license for money creation on behalf of favored groups. They create secret bailouts, currency swaps, and special loan programs worth trillions of US Dollars. For example, the Bank of England, still the central bank of the UK, was founded to support the war machine of the King of England in 1694. And it is now known that actions of the Bank for International Settlements, the central bank of central banks, supported financing for Hitler’s activities, and facilitated Nazi theft of national gold from other countries. It is extremely likely that there would be far less war in the world were it not for central banks printing money in support of the war-making capabilities of national governments.

Regardless of the publicly stated aims of central banks for currency and price stability, full employment, economic growth, and so forth, their actions are easily understood when it is clear that the paramount goal of central banks is to protect the game of the large banks. While nominally they are regulators of large banks, in practice, they support and protect the banking cartel. Thus this power further assures the structural advantage of the banks.

We will return to the topic of central banks in the discussion of fiat money below.

Taxation

Taxation is another major structural unfairness, along multiple lines:

Sheer Size of the Tax Burden: First is the sheer size of taxation in the modern world. As an example, government costs the citizens of Denmark 48% of their country’s Gross Domestic Product, and they are not the only country in which the cost of government is approaching 50% of the nation’s output. Yes, some of the money collected by government is returned to citizens in the form of direct disbursements such as retirement pensions and purchased services such as health care. But much of it funds a permanent bureaucracy, standing military, and interest payments on debt. Can a tax jurisdiction and the individuals within it be prosperous in the long term when government takes nearly half the income of those actually producing goods and services in the economy?

Why is this “sheer size” problem structurally unfair? It is on at least two counts:

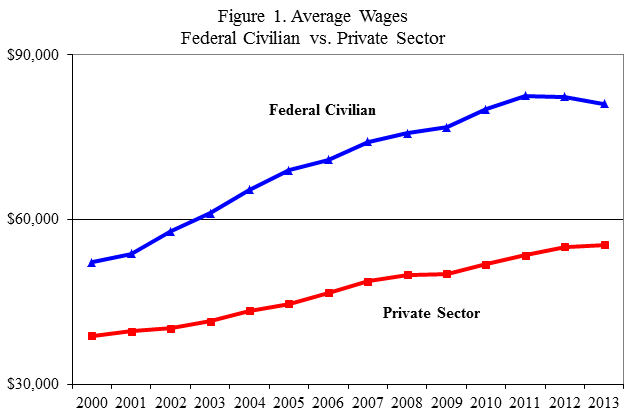

A. Government career employees deciding their own salaries has resulted in a structural unfairness in the US, where average federal civilian compensation is almost twice average private sector compensation:

(Chart source)

(Chart source)

And these compensation statistics do not include the lavish lifestyles and red-carpet treatment politicians and bureaucrats often arrange for themselves at taxpayer expense.

B. Huge taxation results in massive government spending for goods and services. This disproportionately enriches those vendors who secure government contracts, at the expense of other businesses, and at the expense of the taxpaying public. These vendors can use their profits to curry further favor with those in charge of government expenditures, leading to the dreaded “military industrial complex,” “medical industrial complex,” and so forth.

The Legitimacy and Inevitability of Taxes: People have come to accept “death and taxes” as inevitable. While people often argue about the fairness of particular taxes, it is rare to hear a discussion of whether taxes are legitimate at all, despite the fact that this page on the History of tax resistance lists hundreds of tax revolts and rebellions, including famous events such as the American and French Revolutions. Most national boundaries and governments were formed through war, with taxes being promptly levied within the jurisdiction by the victors. Does skill in war make taxing legitimate? Or is it simply imposed by force, particularly with the threat of jail time, without the consent of the governed?

If governments can print money, why are there taxes? If a national government can print money, why do they need to tax at all, why not simply print the money they need? If this question seems absurd or fanciful, here is a paper written in 1946 by the then-president of the US Federal Reserve Bank of New York making precisely that point. He said that if a national currency is not backed by gold or any other commodity, and the national government or its central bank can print the money, then taxes at the national level are unnecessary. He said taxation at that point can be a tool of social and political policy, for example, to “subsidize or penalize various industries or economic groups,” or to implement progressive income or estate taxes to redistribute wealth, but that it is not a necessity. So we need to ask ourselves: what is the true purpose of the large tax burdens currently heaped on citizens?

Taxes Used for Personal Power: Taxation directs a vast and seemingly ever-increasing flow of funds to an entrenched political class that identifies the good of the nation, state, or municipality with their personal retention of power. Increasingly, this political class uses all possible organs of state power—spy agencies, tax agencies, the courts, regulatory agencies, government spending, control of the media, and so forth–to strengthen their personal power by destroying or suppressing opposition. They use state apparatus to attack political opponents, jail whistleblowers, and destroy the lives of dissidents and of capable investigative reporters who refuse to “play the game.” They often claim that those who oppose them are a threat to “national security.”

This power is further enhanced by direction of the flow of tax money to favored supporters and away from opponents through government spending, changes to tax law, loans and loan guarantees, and manipulation of purportedly free markets.

While one would expect this in dictatorships, it has become true in nominal democracies as well.

Secrecy: In addition, parts of the tax collection, government borrowing, and government expenditure processes are shrouded in secrecy, making accountability impossible. Most governments now have “black budgets”–typically related to military and spying operations, the infamous “black ops”–where the amount and purpose of the expenditures is secret. This is a small part of the massive secrecy that shrouds much of government planning and operations, even in nominal democracies. Much of governing today happens “behind closed doors,” and what goes on behind those doors is not revealed for years or decades, if ever.

This secrecy and lack of accountability allows for the theft of trillions of dollars. On rare occasions, this is admitted by government officials, as in this video:

from CBS News of US Defense Secretary Donald Rumsfeld announcing, on the day before the infamous 9/11 attacks, that $2.3 Trillion had gone missing at the Pentagon. (Any mention or tracking the missing $2.3 Trillion disappeared, of course, after the 9/11 attack.) Independent investigators have documented additional trillions that have gone missing from US government coffers.

Worldwide, most are all too familiar with the stories of politicians who arrived in an office of “public service” as a person of modest means who left that office with great wealth.

Market Manipulation Departments: Also in the realm of secrecy, almost all governments have departments funded by taxpayers for the manipulation of supposedly free markets. In the US, this work in centered in the Exchange Stabilization Fund of the US Treasury. The actions and trading profits of these departments are almost invariably hidden from public scrutiny. Which markets they manipulate and when they do so is rarely revealed, offering ample opportunity for abuse in terms of cementing the personal power of entrenched politicians and the advantage of favored constituencies.

The Tax Avoidance Game: Large and complex taxation regimes lead to businesses and individuals putting great effort into avoiding taxes. Rather than deploying resources in the most logical and productive way, many make decisions based on tax consequences instead. Entire industries exist to help them find loopholes, tax advantages, tax deferrals, off-shore tax havens, and strategies and tactics whose legality is sometimes questionable at best. Businesses and individuals struggle through a blizzard of tax forms, regulations, and audits to pay as little as possible in taxes rather than spending their precious time and resources on productive and life-enhancing activities. Huge government bureaucracies exist solely to collect, interpret, and enforce large and ever-growing tax codes, often now assisted by national spy agencies and law enforcement agencies who are “following the money” and can provide mountains of information about the financial behaviors of the populace.

Taxes that strongly benefit the money creators: In many countries, interest expense on business loans and mortgages is tax deductible. This is a huge incentive for companies and individuals to take on debt, thus super-charging the flow of interest expenses into the hands of those who have large sums of money to lend, especially the money creators, the banks. Just in the US in 2015, from corporate announcements, it is expected that companies will purchase over $1 Trillion of their own company stock from the public market. For many companies, all of this stock buying is funded by new debt. This drives up the stock price of the company and the interest expense is deductible. So rather than investing their money in productive activities, companies deploy vast sums in so-called financial engineering, which is a polite term for gaming the system.

Summary on Taxation: Taken together, taxation–grudgingly accepted by most in part because of its ballyhooed noble aims and inevitability–has been hijacked by a small class of people, government and private, to assure the increasing vastness of their wealth at the expense of the rest of society. It is as though this small group has steeply tilted the economic table in their direction so that they receive a portion of every economic transaction, of every payment for someone’s labor, and of every payment for every product sold in the society. If we are to vanquish financial problems once and for all, taxation as currently practiced must be understood as a major structural unfairness and impediment, and every avenue for its complete elimination must be explored.

But wait. . . There’s more. Here is Part 2.

Pingback: The Current System is PURPOSE-BUILT for Extreme Wealth Disparity, Draft Part 2 | Thundering Heard

Pingback: The Current System is PURPOSE-BUILT for Extreme Wealth Disparity, Draft Part 3 | Thundering Heard

Dear Thundering Heard,

Brilliant job! Just one comment on the section titled “Structural Unfairness, the Details”, fourth line: “And the trend toward of extreme wealth “, I believe the “of” may be a typing error.

Thank you for keeping your finger on the pulse!

Van

Hello Van,

Thanks very much for the kind words and for the careful reading that revealed the wording error you pointed out, it has now been fixed.

TH