The insatiable banking/corporate/political crony network that has stolen so much from people in the past has some new schemes in store. First on the docket is the bail-in, where reckless banks with huge losses will be kept afloat not by the general base of taxpayers, but by those who have lent them money. And as mentioned in Update on Metals, Deposit Confiscation, and Capital Controls, depositors are definitely grouped into the class of those who have “lent” money to these banks. As in Cyprus, if a bank fails and the regulators decide that depositor money will be confiscated, the depositors receive some stock in the bank in exchange for their money. We’ll see later in this post just how well that is working out for people in Cyprus. But first, let’s establish that bail-ins are definitely the new thing:

It Can Happen Here: The Confiscation Scheme Planned for US and UK Depositors

Confiscating the customer deposits in Cyprus banks, it seems, was not a one-off, desperate idea of a few Eurozone “troika” officials scrambling to salvage their balance sheets. A joint paper by the US Federal Deposit Insurance Corporation and the Bank of England dated December 10, 2012, shows that these plans have been long in the making; that they originated with the G20 Financial Stability Board in Basel, Switzerland (discussed earlier here); and that the result will be to deliver clear title to the banks of depositor funds…

Although few depositors realize it, legally the bank owns the depositor’s funds as soon as they are put in the bank. Our money becomes the bank’s, and we become unsecured creditors holding IOUs or promises to pay. (See here and here.) But until now the bank has been obligated to pay the money back on demand in the form of cash. Under the FDIC-BOE plan, our IOUs will be converted into “bank equity.” The bank will get the money and we will get stock in the bank. With any luck we may be able to sell the stock to someone else, but when and at what price?…

No exception is indicated for “insured deposits” in the U.S., meaning those under $250,000, the deposits we thought were protected by FDIC insurance. This can hardly be an oversight, since it is the FDIC that is issuing the directive.

Wealthy bank depositors to suffer losses in EU law

A draft European Union law voted on Monday would shield small depositors from losing their savings in bank rescues, but customers with over 100,000 euros in savings when a bank failed could suffer losses.

Asmussen clarifies EU Parliament: savers must bleed for bank rescue

Japan to adopt ‘bail-ins,’ force bank losses on investors if needed, Nikkei says

Land Of The Rising Bail In: Deposit Confiscation Coming To Japan Next

Other countries have hopped on the bail-in bandwagon, but you get the idea.

To absolutely confirm that bail-ins are coming, the next story is about an organization called ISDA preparing for how to handle bail-ins. Why is this important? Because the following is a list of the voting members of the ISDA Determinations Committee:

- Bank of America N.A.

- Barclays Bank plc

- BNP Paribas

- Citibank, N.A.

- Credit Suisse International

- Deutsche Bank AG

- Goldman Sachs International

- JPMorgan Chase Bank, N.A.

- Morgan Stanley & Co. International plc

- UBS AG

That is the rogues gallery of derivatives trading on this planet. And what is this Determinations Committee determining? Who gets what on all of the derivative bets placed with respect to any bank that gets a bail-in. In other words, there will be bets that the bank will fail, bets that the bank will survive, bets on the bank’s bonds, etc. etc., and these guys are now setting the rules for who gets what after a bail-in. If these folks think it’s necessary to protect themselves relating to bail-ins, then gee, I wonder if everyone else ought to do the same?:

New CDS trigger event proposed to tackle bail-in

ISDA is consulting on a proposal to add another credit event for financial credit default swaps in order to adapt to sweeping changes in regulation that will give supervisory authorities the power to bail-in the debt of floundering institutions.

For further proof, those who are well-connected are already working to make sure that they are exempt from the torture of a bail-in:

EACH wants CCP exemption from bail-ins

Rest assured that there will be bank failures because the big ones have gone back to the methods that precipitated the financial crisis on the first place. They are again selling CDOs, one of the primary culprits in 2008:

‘Frankenstein’ CDOs twitch back to life

And they are once again granting what are called “covenant-lite” loans.

And in new depths of scum-sucking bottom-feeding, banks are so desperate for capital and profits and bonuses that they are now pursuing people upon whom they foreclosed to make up the difference between the mortgage loan amount and the price the banks were able to get for the house when they sold that house after foreclosure:

Lenders seek court actions against homeowners years after foreclosure

For Jose Santos Benavides, the ordeal of losing his home was over.

The Salvadoran immigrant had worked for years as a self-employed landscaper to make a $15,000 down payment on a four-bedroom house in Rockville. He had achieved a portion of the American dream, earning nearly six figures.

Then the economy soured, and lean paychecks turned into late mortgage payments. On Aug. 20, 2008, one year after he bought his dream home for $469,000, the bank’s threat to take his house became real via a letter in the mail. Just four days before the bank seized the property, he moved out, along with his wife and their two young children.

That wasn’t the worst of it.

In November, more than three years after the foreclosure, he was stunned to learn he still owed $115,000 — with the interest alone growing at a rate high enough to lease a luxury car.

“I’m scared, you know,” Benavides said. “I can’t pay.”

The 42-year-old is among the many homeowners being taken to court by their lenders long after their houses were taken in foreclosure. Lenders are filing new motions in old foreclosure lawsuits and hiring debt collectors to pursue leftover debt, plus court fees, attorneys’ fees and tens of thousands in interest that had been accruing for years.

From that Washington Post article, here is a chart that shows that, in some states of the US, the banks have 40 or more years after the foreclosure to go after former “homeowners” upon whom they foreclosed:

So the banks engaged for years in seriously questionable lending practices, packaged up mortgages they knew would fail into “securities” that they sold all over the world, created fake documents and had them robo-signed to accomplish foreclosures, and now they can hound people for decades for what the banks say are their losses on these mortgages. With interest. And attorneys fees. I wonder who created such a legal system. As Bank of America employees reported:

So the banks engaged for years in seriously questionable lending practices, packaged up mortgages they knew would fail into “securities” that they sold all over the world, created fake documents and had them robo-signed to accomplish foreclosures, and now they can hound people for decades for what the banks say are their losses on these mortgages. With interest. And attorneys fees. I wonder who created such a legal system. As Bank of America employees reported:

‘We were told to lie’ – Bank of America employees open up about foreclosure practices

Employees of Bank of America say they were encouraged to lie to customers and were even rewarded for foreclosing on homes, staffers of the financial giant claim in new court documents…

“To justify the denials, employees produced fictitious reasons, for instance saying the homeowner had not sent in the required documents, when in actuality, they had,” William Wilson, Jr., a former underwriter for the bank, wrote in his statement.

As a side note on Europe, rumor has it that the infamous EU Finance Minister Jeroen Dijsellbloem, the one who correctly stated in public that the Cyprus bank action was a template for future bank resolutions, is pressing EU officials to try to preemptively resolve the problem of insolvent EU banks via deposit confiscation. And he wants to do that soon. So far, all attempts to fix EU bank problems have been band-aids that temporarily covered over the real problems; none have come close to a real solution, and we’ll get to the reason for that below. But if you have any notion that EU banks are solvent, then read this comment about Deutsche Bank by a former US Federal Reserve Bank President:

Deutsche Bank “Is Horribly Undercapitalized… It’s Ridiculous” Says Former Fed President Hoenig

A top U.S. banking regulator called Deutsche Bank’s capital levels “horrible” and said it is the worst on a list of global banks based on one measurement of leverage ratios. “It’s horrible, I mean they’re horribly undercapitalized,” said Federal Deposit Insurance Corp Vice Chairman Thomas Hoenig in an interview. “They have no margin of error.” Deutsche’s leverage ratio stood at 1.63 percent, according to Hoenig’s numbers, which are based on European IFRS accounting rules as of the end of 2012.

Deutsche Bank is the biggest player in the world in the risk-laden derivatives market. At last count, they had $73 trillion in derivatives outstanding, which is over twenty times the size of the German GDP, so if Deutsche Bank has a derivatives blow up, it’s unlikely that Germany or anyone else would be able to afford to make good on their losses. After all, $73 trillion is larger than the entire world GDP.

And why is it that, as stated above, there have been no attempts to really solve EU bank problems? It’s very simple: too much debt was issued to buy assets (e.g., real estate), pushing up the price of those assets to unrealistic levels. There are real losses that need to be taken, and no one wants to take the losses. All involved prefer to pretend that there are no such losses, so they use near-zero-interest bridge loans, accounting lies, and round robin I’ll-lend-your-bank-money-to-buy-your-government-debt-and-you-use-the-proceeds-to-bail-out-your-bank games to mask the truth. With non-performing loans at EU banks at record highs and growing by the day, good luck with that.

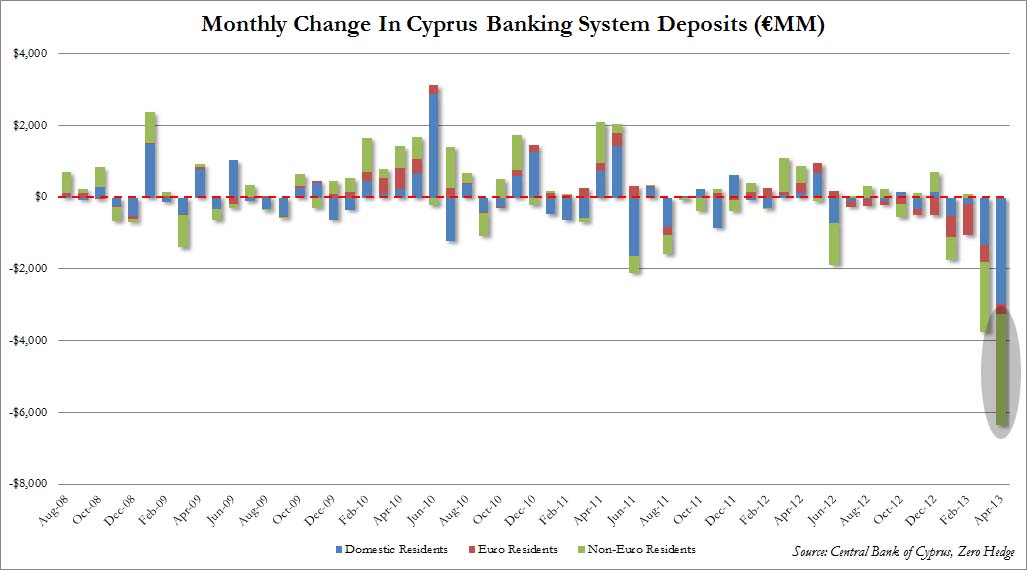

But here is the problem with bail-ins, the latest and great “fix” for the financial system: so far, they don’t work. Let’s look at the infamous Cyprus case: they stole a lot of deposits and in return, gave people stock in the bank. But few want to keep their money in that bank anymore. Even with strong limits on daily withdrawals from the Cyprus banks, people are persistently removing their money from those banks:

Cyprus Bank Deposits Plunge By Most Ever During “Capital Controls” Month

Here’s what the trend of withdrawals from the Cyprus banks look like:

That’s more than $6 billion being withdrawn in April, after the March bail-in. So that bank stock that people received in return for their “expropriated” deposits? Must be worth a fortune. If people still received stock certificates as a matter of course, at least these could be framed as memorabilia, yet another testament to the financial follies of humanity. But it’s all just electronic entries these days. Switch a few bits and bytes and then who owns what?

And the whole Cyprus action is breaking down anyway:

The Cyprus Bail-In Blows Up: President Urges Complete Bailout Overhaul

Cyprus’ President Nicos Anastasiades has realized (as we warned), too late it seems for the thousands of domestic and foreign depositors who were sacrificed at the alter of monetary union, that the TROIKA’s terms are “too onerous.” Anastasiades has asked EU lenders to unwind the complex restructuring and partial merger of its two largest banks…

Not that the bail-outs actually worked either. Despite the fact that the EU leaders touted each of the first three Greek bailouts as the final fix, Greece now needs a fourth:

Greece Has One Month To Plug A €1.2 Billion Healthcare Budget Hole

Think Cyprus is the only country that will need a repeat bailout (as the FT reported earlier)? Think again. Cause heeeeere’s Greece… again…. where as Kathimerini reports, a brand new, massive budget hole for €1.2 billion has just been “discovered.

And here’s another nice theft tactic. Well, nice if you are the bank. The Bank of Ireland just doubled the interest rate on existing floating rate mortgages where the fine print allowed them to do so:

Bank Of Ireland Doubles Mortgage Rates, Homeowners Fear More To Come

And expect to hear a good deal more about wealth taxes in the coming months:

German ‘Wise Men’ push for wealth seizure

Professors Lars Feld and Peter Bofinger said states in trouble must pay more for their own salvation, arguing that there is enough wealth in homes and private assets across the Mediterranean to cover bail-out costs. “The rich must give up part of their wealth over the next ten years,” said Prof Bofinger.

And last but not least, you know all that money sitting in retirements accounts? Multiple countries have nationalized such accounts in recent years. People like former Republican Administration insider Catherine Austin Fitts have been warning people that US politicians salivate when they contemplate getting their hands on that pool of $18 trillion.

OK, just three final (brief!) comments:

1. You’ve heard the old saying about someone who “wants your money in their pocket.” The problem here is most people’s money is already stored in “their pocket,” that is, it’s already being held by the institutions that want to grab it.

2. That thing about the banks going after people for more money after they have already foreclosed on them? Too bad we don’t have a Charles Dickens around to dramatize this type of behavior, maybe then people would get the depth of depravity in this system.

3. Tread carefully out there, folks, it looks like acceleration spares nothing, so I think you want to be real careful about “wait and see.” You know my view: banks are for transaction accounts, not savings.

Next time we’ll cover another big pile of electronic money, brokerage accounts.

Pingback: It’s Bail-In time | Thundering-Heard