Yet another instance of the accelerating flood cycle: a photo from the devastating Himalayan floods, indicating a stance people might wish to take during these times:

* * *

Despite being surrounded by the cyclic nature of physical life (breathing, heartbeat, blinking, day/night, tides, seasons, birth/death … and the less visible or invisible: sound waves, radio waves, x-rays, microwave cooking, evolution … and for a fun contemplation of large astronomical cycles, see this and this), for the most part, people tend to ignore cyclicality in favor of seeing life as a straight-line progression. This is unfortunate for at least two reasons: first, because all form is cyclic—form emerges, flourishes to some extent, and dissolves; second, because there are some not-so-obvious cycles that offer understanding for what is otherwise quite mysterious. In fact, here at Thundering Heard, we are on a path to discuss the biggest cycle of them all for people, a cycle that, once grasped, contains the answers to “little” questions like the meaning of life, why are we here, and so forth. But first, let’s get more adept at seeing the cyclic aspect of life and how important it is.

The Sunspot Cycle

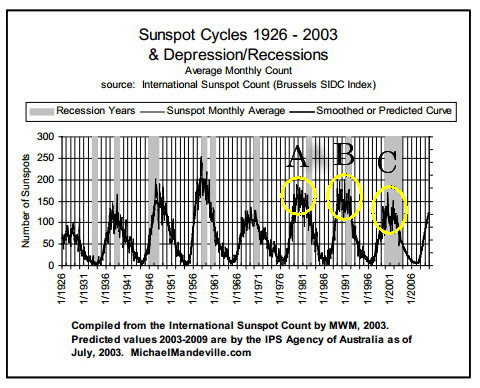

There is a peak of sunspot activity every 10 to 13 years, with 11 years being the average for each cycle. A chart of the peaks and troughs of sunspot activity from 1926 to 2009 looks like this:

Let’s look at the three peaks labeled A, B, and C.

The peaks of sunspot activity often really “rev people up” financially, that is, there is typically an excitation of human activity that leads to a financial market bubble that coincides with the sunspot peak.

Three peaks ago, the peak in 1980, labeled A above, coincided with the peak of the commodity price boom and price inflation that took place in the 1970s after Nixon defaulted on the US promise, made near the end of World War 2, to always support conversion of Dollars into gold. Those were the days when the so-called Misery Index (inflation plus the unemployment rate) was tracked in daily newspapers, and mortgage rates in the US rose to 18%.

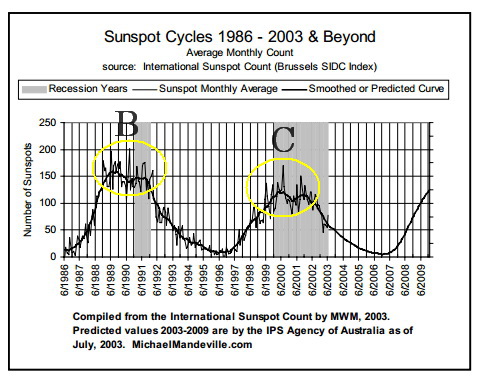

Here’s a closer look at the last two peaks of sunspot cycle activity:

The cycle peak labeled B was in 1990 and corresponded with the peak in Japan of bubbles in their stock and real estate markets. This was the time when it was generally held that Japan Inc. would rule the world, or at least own it; that its economy would soon be the largest in the world. A single block of downtown Tokyo real estate was said to be worth more than all of the real estate in California. Now that’s a bubble! (We’ll see in our next post on cycles why that Japan bubble grew so large when we cover another cycle that also contributed to this Japan peak. When multiple important cycles converge, the results can be gargantuan.) Following that peak, Japan experienced what has come to be called The Lost Decade, though it has now run for two decades. Both their stock and real estate markets lost 75% of their “value” after that peak, and they still have not come anywhere close to recovering their former glory as Japan has been mired in nearly constant recession ever since.

The sunspot peak labeled C aligned with the peak in the internet/technology stocks in the Spring and Summer of 2000, another famous bubble. Again money flowed, this time into Pets.com, Webvan,com, Geocities,com, DrKoop.com, and many others, most of which had little going for them except an idea and a web site. Little or no sales, no profits—who cared! They were going to the moon. It was a New Paradigm. If you thought it was insane, you “just didn’t get it.” And the thing is, that craziness for internet stocks had been in play for a few years; that hoopla could have ended in 1998 or 1999. But it didn’t. It ended when the sunspot cycle peaked in 2000.

Looking back, it would have been great for the participants in those bubbles to be aware of the sunspot cycle peak. They could have sidestepped a lot of trouble. So what’s going to happen this time around? Well, for a few years, I have thought that this economic cycle might hang on into the peak of the current sunspot cycle, called Solar Cycle 24, which was projected for August 2013. But Amon Ra may have thrown us a curve ball. It looks like this cycle will not have the usual single large peak, but rather a dual peak like Solar Cycle 14 from the early 20th Century. According to solar physicist Dean Pesnell of NASA’s Goddard Space Flight Center:

“This is solar maximum. But it looks different from what we expected because it is double peaked.” Pesnell noted similarities between the current cycle and Solar Cycle 14, which happened between February 1902 and August 1913 and experienced a double peak. If the two cycles are in fact twins, he said that “it would mean one peak in late 2013 and another in 2015.”

Here is a chart that shows the peak in 2000 plus our current cycle:

If the NASA guy is right, there should be a bubble peak in either 2013 or 2015. But a bubble in what? Here are some clues:

- Lots of savings accounts pay only 0.01% in interest.

- Mortgage rates got near 1% in Japan and 3% in the US. (Would you lend money to a stranger for 30 years for 3% interest? Neither would banks, which is why almost all mortgages need a guarantee from a government program or the banks won’t make the loan.)

- Short-term interest rates in Germany and Switzerland recently went negative. That’s right, if you wanted to lend money to Germany or Switzerland on a short term basis, you had the pay them for the privilege.

If you think these phenomena don’t make a lot of sense, you are right. But it points to the culprit that has all the hallmarks of a monster bubble: the world government bond market. The bull market in bonds has been running for over 30 years. On May 2, if you wanted to lend money to Germany for 10 years, they would pay you an interest rate of 1.2%; the US, 1.6%. And if you wanted to lend Switzerland money for 10 years in December, they were paying a whopping 0.4%. Japan? 0.45%.

And in the case of Japan in particular, they are working very hard to devalue their currency, to make sure the yen falls in value. So the question is, who in their right mind would lend to these countries for such a pittance in interest, especially while most of them are printing money to intentionally debase the value of their currencies!?! You get a very poor interest rate and, if you get your capital back, it will be in a currency that will have fallen in value over 10 years. Yet, that is what institutions and people are doing. Recently, if you wanted to get a reasonable interest rate on 10-year government bonds, then you would have lend money to the country of Rwanda; they paid 7% on a recent offering of 10 year bonds. Best of luck getting your capital back 10 years from now.

When this bubble bursts, the consequences will be huge. This is not a bubble in one country, like Japan in 1980, or in one sector of the economy, like tech stocks in 2000, we’re talking about government bonds, worldwide! This is the market that supports military spending, education, transportation, and just about every safety net (in the US: Social Security, Medicare, Food Stamps, Medicaid, Unemployment Insurance, and so forth) on the planet. And you get this paltry interest rate when you might not even get your capital back in 10 years. A number of governments are on a clear trajectory for bankruptcy; there is a good chance that bond buyers will not get their capital back! And yet they lend huge amounts of money to these governments. Especially Baby Boomers, they have been pouring money into bond funds. Just like they poured money into stocks in 2000, and real estate investments in 2006. Oh well.

When do I think the bond bubble will pop? This year! 2013. I don’t think it can last to 2015. In fact, the bubble pop may have already started. And guess which institutions count government bonds as their major “stable” capital: banks. Yet another reason to watch out for the banks!

Furthermore, the solar cycle might actually peak this year. The NASA guy might be wrong about the dual-peak forecast.

What will it mean if this bubble pops? It means interest rates will rise, possibly a lot. This will strongly increase the amount of interest governments must pay on their debts. Their deficits will skyrocket.

Mortgage interest rates are closely tied to the government bond market, so mortgage rates will rise as well. (US mortgage rates rose from 3.88% to 4.35% just over the last week!) And if government deficits skyrocket, programs will need to be cut, so the massive support they are currently providing for the mortgage market will be in jeopardy, threatening even further rate increases.

Still, two cycles that we will discuss in the next post about cycles argue for that 2015 date.

* * *

I would like to make one thing very clear: If you woke up tomorrow and heard that a large “systemically important” international bank had collapsed, causing chaos in the rest of the financial system, and that most banks would be closed for some number of days, would you really be surprised? Probably not. Many people are starting to get the idea that the system is not exactly solid. I am certainly in that camp. So when I talk about August 2013 or some month in 2015 as the month when the real systemic collapse will commence, please know that, in my view, the more-than-sufficient conditions are in place for that full system collapse to happen at any minute. Discussions like the one above are an attempt to get a handle on probabilities. In terms of preparation, acceleration is not to be trifled with: I think that everyone should be doing what they can to be prepared now. If it turns out there is more time for preparation, fabulous, this type of preparation takes awhile and I’m sure we can all use the time. But that time may be short indeed. As the photo at the top of the post shows, when change arrives in your area, it may be monumental change.